SAFE + Token Warrant: Understanding the Meta, Part 2

This blog post analyzes the differences between SAFT and SAFE + token warrant; the different token warrant models; the models' impact on valuation, tokenomics & governance.

This is Part 2 of our blog post on the SAFE + Token Warrant meta. You can find Part 1 here.

This blog post will address two key issues in structuring crypto VC deals: (i) should you use a SAFE + Token Warrant or a SAFT? and (ii) if you use a SAFE + Token Warrant, what should the terms of the token warrant look like?

SAFT vs Token Warrant

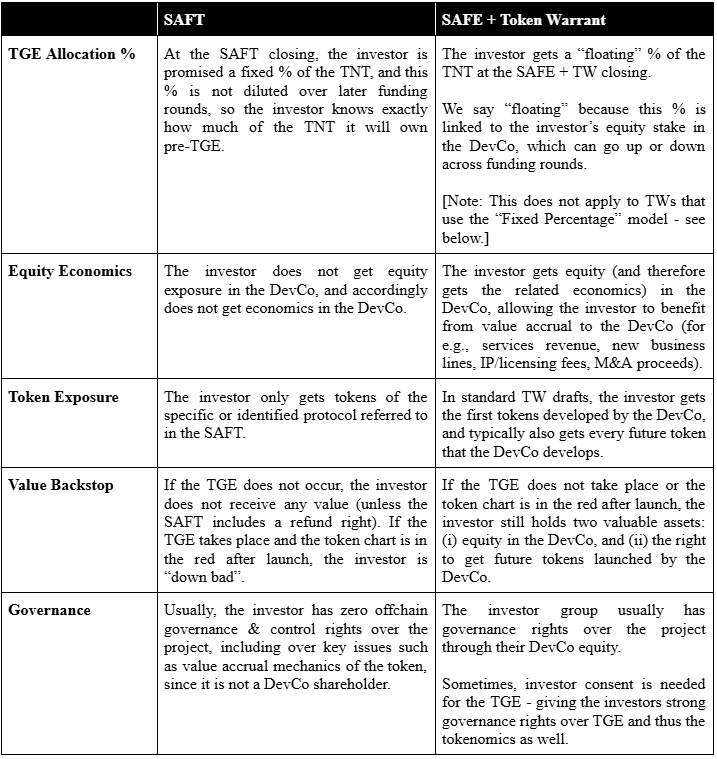

SAFT

The Simple Agreement for Future Tokens (“SAFT”) was formalized in October 2017 via The SAFT Project whitepaper12. The development company of pre-TGE token projects (“DevCo”) issues a SAFT to raise capital, with tokens to be delivered to investors after the token generation event (“TGE”).

During the “ICO Boom”, crypto was nascent and since the SAFT did not involve any equity funding, DevCos used SAFTs for high speed, low friction, cross-border fundraising from retail, institutional investors, investment DAOs etc. Projects had a lot of negotiating leverage due to the fierce competition for allocation, so the market saw structured SAFT fundraises with differing prices, discounts, and lockups (for example, Filecoin’s 2017 raise345 and Telegram’s two-round sale67).

The core commercial of the SAFT is:

“in exchange for giving me USD X, I will give you Y% of the protocol’s total network tokens (“TNT”) at a price of USD Z per token, if the TGE takes place”.

With no equity shares in the DevCo and limited negotiating power, SAFT investors usually had zero governance rights. They soon realized that this left them exposed to the following risks: token design risk (no effective remedy if the token did not turn out to be what investors were promised), execution risk (no effective remedy if the DevCo did not do a TGE, but “rug pulled” instead), and delivery risk (no effective remedy if TGE took place, but investors did not get tokens).

Token Warrant

The token warrant (“TW”) became popular from 2021 onward during the “regulation by enforcement” phase of crypto8.

In contrast to a SAFT (which is essentially a right to receive a slice of the TNT once a TGE takes place) a TW accompanied an equity investment in the project’s DevCo. The equity investment was either through a SAFE or a “priced” equity round.

The core commercial of the TW is:

“in exchange for buying X% of my DevCo’s equity, we will apply a formula to X% and derive Y, and at the TGE you will get Y% of the TNT for a nominal price”.

Different kinds of formulae (which we call “TW models”) are used. We will discuss the different TW models in more detail below.

Differences

So what are the differences between a SAFT and a TW from an investor perspective?

Takeaways

Here are our takeaways from the above comparison:

Firstly, the SAFE + TW has become popular amongst VCs because it hedges the two big commercial risks in early stage crypto deals: business pivots and “first token” risk. From a venture investing perspective, given the rapid pace of innovation (and its interplay with meta and mindshare in the crypto space) this makes sense. Since most startups eventually pivot, why should an investor be locked-in to a deal where they only get the economic upside of the v1 product iteration of a startup?

In a retrospective study of the 2022 cohort of seed stage projects, Lattice Fund found that while 72% of them launched on a mainnet by 2024, only 15% of them launched a token9. Given VCs’ fiduciary duties to their LPs, this statistic suggests that VCs should hedge by getting equity in the DevCo in every deal.

However, by preferring the SAFE + TW structure, investors sacrifice the SAFT’s key commercial feature: it gives investors a “non-dilutable token allocation”. VCs seem to have (by and large) made peace with letting this feature go and trading it for the SAFE + TW structure for reasons mentioned above.

Secondly, which deal structure works better is often contextual. These are our notes on which structure to use:

A SAFE + TW structure is best suited for early stage projects with a fuzzy roadmap that are yet to define their tokenomics (i.e., the economic characteristics of the token, including its supply, distribution, utility and value accrual). By using the TW structure, projects can raise using equity and retain flexibility to launch a token (or not). By using certain kinds of TW models (see below) founders can also get more flexibility in structuring tokenomics than they would with a SAFT.

A SAFT structure is more appropriate for mature projects which have a well-defined protocol design and tokenomics and with a clear roadmap to a TGE. Since the project is mature, the SAFT can be priced at an explicit fully diluted valuation (“FDV”).

The above are rough rules of thumb. For example, pre-TGE Layer-1s might have clear tokenomics and a roadmap to TGE, yet Layer-1 funding rounds are often enormous in $ terms - so investors want strong governance rights on account of the huge amount of capital at risk. To get these rights, they structure the deals as SAFEs + TW (with the governance terms in a side letter) or priced equity rounds + TW (for example, the Aptos & Monad fundraises; but as a counter, Berachain has raised large rounds using the SAFT).

There is no clear winner in terms of which deal structure is more dilutive - it is very path-dependent for each project. Some dynamics to consider here: (i) projects sometimes need very little financing before going to TGE, meaning that early investors do not get heavily diluted - to illustrate, Renzo timed the LRT meta when it was hot and raised just USD 20M (seed + series A) before rolling out a TGE, giving their VCs ~31% of the TNT, and (ii) SAFT rounds are typically priced higher to account for the dilution that comes from team, treasury, and community airdrop allocations. Net effect: outcomes hinge on more than just the deal structure.

Beyond the legal & commercial issues highlighted here, these deal structures also have other impacts (including signalling, founder-investor-community alignment, etc.) and these have been well noted by founders and investors alike.

Thirdly, and to borrow a clip from Jeff Bezos’ famous Lex Friedman podcast episode, we don’t believe that using a SAFT structure is a “one way door” to a token-only model for a project’s trajectory.

We have seen projects where the initial raise was on a SAFT, and later rounds were done using a SAFE + TW (with early investors swapping their SAFTs for SAFE + TWs); note that this optionality is only available to founders, not investors - a SAFT investor is legally & contractually (but not practically) powerless to demand equity in the DevCo if it looks like the DevCo equity will accrue more value than the token.

We have also seen projects raise using a SAFE + TW for a few rounds and then do pre-TGE rounds using a SAFT, because at that point, it made more sense to use a SAFT and onboard investors who are more crypto-native.

Fourthly, the jury is out on which of these two deal structures is more beneficial for founders. While using a SAFT helps founders retain control & economics in their DevCo, and ensures they need not give the “second” token they develop to their early investors, the “non-dilutable token allocation” is a bug because it potentially compresses token allocations for the founders, team, treasury, ecosystem and community airdrop. This is a difficult structuring choice for founders. We believe that this choice will be increasingly dictated by investors, especially if sophisticated investors are involved (the exception being highly competitive or “hot” funding rounds). These investors will choose the SAFE + TW structure.

Token Warrant Models

Given the popularity of the SAFE + TW structure, let’s now analyze the TW models. The model determines how much of the TNT the investor will receive, so it is the most negotiated and engineered issue in a TW.

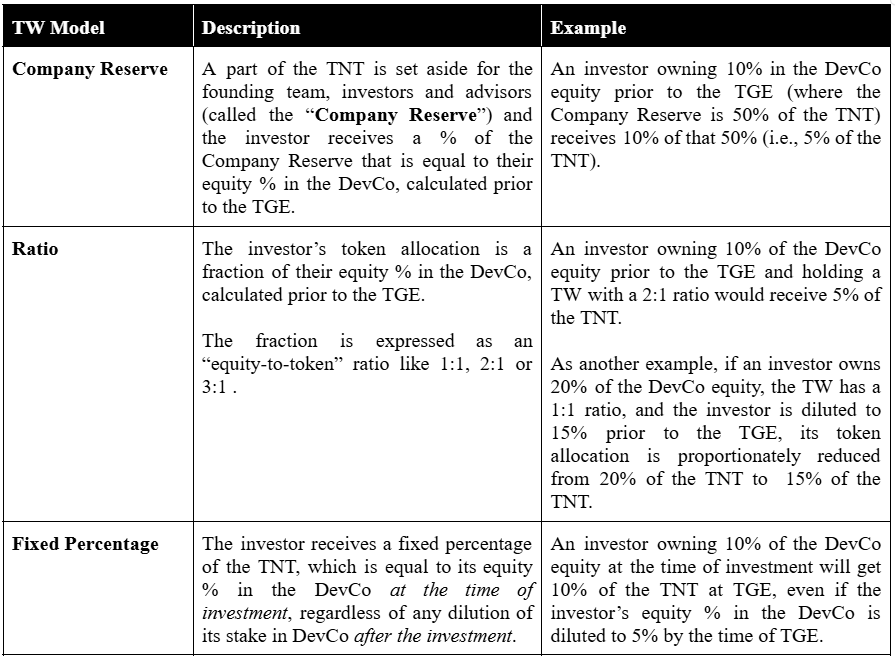

These are the three popularly used TW models:

Implications

What are the implications of the TW models? We can divide the implications into three streams: valuation, tokenomics, and governance. Needless to add, these areas are interrelated.

Valuation

An investor’s token allocation from a particular funding round depends on the TW model used in that deal. Therefore, we can use the TW model to derive the FDV of the token at the time of the funding round. For example, in an equity funding round at a USD 10M post-money valuation, where the TW has a 2:1 ratio, the investor is effectively buying the tokens at a USD 20M FDV.

This is a fairly linear and straightforward mathematical relationship, but there are a few nuances beyond the numbers to consider:

TWs sometimes use the “Company Reserve” model, but do not specify how much the “Company Reserve” will be (it is fixed later on, but prior to TGE). While this variant of the “Company Reserve” model gives some flexibility on structuring tokenomics (discussed below), there is a governance trade-off (also discussed below), as well as a valuation issue: the investor does not know its entry FDV (i.e., the FDV depends on the allocation, which in turn is linked to the size of the Company Reserve - which is not fixed). Price sensitive investors will not like this uncertainty around FDV because it makes it difficult for the investor to decide whether a particular deal is the best deployment of capital at that point in time. It is also not ideal for founders to have only a vague idea of how much of the project’s token supply has been given to that particular investor.

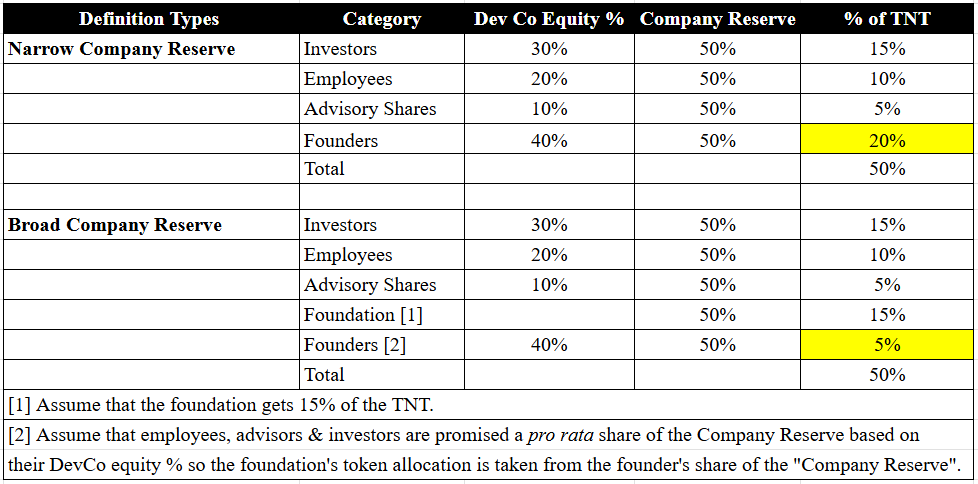

How the term “Company Reserve” is defined (i.e., broadly to include the project foundation’s token allocation, or narrowly without including the foundation’s allocation) can impact the founder’s dilution. If “Company Reserve” includes anyone who is not on the equity cap table of the Dev Co, the founders’ token allocation gets reduced - see illustration below.

The “Ratio” model and the “Company Reserve” model can yield the same commercial results for investors. For example, using the “Ratio” model with a 2:1 ratio and a “Company Reserve” model with the Company Reserve set at 50% of the TNT will give the same economic outcome for an investor, purely from a valuation and token allocation perspective.

In economic terms, the “Fixed Percentage” model gives the same result as using a SAFT (i.e., a “non-dilutive token allocation” until TGE). It is not a good idea for founders to issue TWs with the “Fixed Percentage” model, and a16z Crypto correctly terms this as predatory10. We agree with this view since (i) such terms are extremely difficult to renegotiate in a future round, and (ii) it can result in the founding team having very low token allocation, which is effectively the same as saying they raised at very low FDVs and diluted heavily.

Tokenomics

The TW impacts tokenomics because it sets the formula for determining a (potentially significant) portion of the token allocation, and may also set up the governance terms which must be followed to decide the rest of the token allocation.

Therefore, issuing a TW requires founders to start thinking about and piecing together elements of the project’s tokenomics at the pre-seed/seed stage (which is not always ideal since it could be pre-mature and projects are prone to pivots).

Keeping this in mind, which outcomes should founders optimize for on the tokenomics side when negotiating TWs? Our take:

Maximum token allocations for the founders and the team (including future hires), insulated from investor interference.

Sustainable token allocations for the project’s future requirements (including treasury, marketing, community and growth) after insider token allocations are accounted for (which sometimes requires the founders or the investors to scale back their own token allocations).

Autonomy to decide the other tokenomics aspects of the project (such as staking, fee switches, incentives etc.), insulated from investor interference.

The simple guidance here is that founders should use a TW model that results in lesser dilution, thus creating more room for structuring tokenomics in the future (for example, negotiating for a higher ratio, like 2:1 or 3:1). Founders should also note the following nuances when considering the TW’s effect on tokenomics:

If a project issues TWs with a 1:1 ratio and dilutes ~40% of the DevCo’s equity, this usually results in unsustainable tokenomics, since it just leaves ~60% for the founding team as well as the project’s growth post TGE. In such situations, the choice of the “Ratio” model effectively gives the investors a veto right over the TGE, since the project cannot TGE unless investors agree to reduce their allocations (which they are not economically incentivized to do), and this effectively means the TGE is subject to investor consent. Contrast this to a TW using a 2:1 ratio, which would result in ~80% of the TNT being left for the founding team & project needs post-TGE.

If a TW has a 1:1 ratio or uses the “Fixed Percentage” model, it generally trends toward higher investor allocation and can result in (i) the perception (and probably the reality) that founding team is not well incentivized, (ii) the perception that the tokenomics are very “insider heavy”, and (iii) the founding team “squeezing” the community, airdrop and treasury allocations in order to get more tokens for themselves.

While using the “Company Reserve” model may be attractive since it allows everyone to agree on the total insider allocation early on, it is actually/practically difficult to freeze this aspect of the tokenomics at the pre-seed/seed stage. To solve for this, a variant of the “Company Reserve” model should be used where the actual number of the “Company Reserve” is decided later on (but prior to TGE) by the founder(s), or the DevCo’s board, or with investor consent, and/or subject to a range (like 30% to 50%), and/or subject to a floor or cap (like 40%). This variant of the “Company Reserve” model gives founders some flexibility when structuring tokenomics.

Governance

In pre-TGE crypto VC, perhaps the most important application of (and negotiation on) governance is on how a project’s TGE and tokenomics are structured. Note that some value accrual matters (such as the staking and yield mechanism) can be decided pre-TGE but others (such as turning on the protocol’s fee switch, token buybacks/burns) are usually determined via onchain voting post-TGE.

So what are the negotiation approaches available to founders when negotiating governance over the project’s TGE/tokenomics?

One approach is: the project’s tokenomics is a corporate governance matter, to be decided together by the founders and investors, using a market standard voting mechanism or a combination thereof (including board majority, investor majority, class/series voting, board + investor majority etc.).

Another approach is: the project’s tokenomics is a commercial/business matter and therefore investors should not have any decisive say in it (after all, investors can negotiate their token allocation when they initially invest, so they do not need to be concerned about the token allocations of other stakeholders).

A middle ground or hybrid approach might have two prongs: (i) all investors should have the same TW model (discussed further below - see the “MFN Right”), and/or (ii) the founder and team token allocation model should be the same as the investor’s TW model. Beyond these two points, investors should not have any control over tokenomics.

The governance terms of TWs usually reflect one of the above three approaches.

Why do investors want these governance rights? Here are some reasons:

Investors want to ensure that they are being treated fairly compared to other investors. For example, if a later stage investor gets a more favorable “Ratio” than an early stage investor, the early stage investors will see this as unfair because an investor who is coming in at a more de-risked stage of the project is getting better economic terms on the token side.

Investors do not want founders to inconspicuously grant “advisory” token allocations to just a few investors, without any substantial advisory services being rendered for the “advisory” tokens.

Investors do not want founders to be able to unilaterally allocate “bonus” tokens to themselves because this enables extractive self-dealing by founders. Another reason for this is: if founders can allocate “bonus” tokens to themselves, then founders are less incentivized to raise at higher valuations - they might be okay with lower valuations because they know they can offset the dilution later on. To draw a parallel, in mature/unicorn web2 companies there is always tight governance around whether founders can grant themselves more stock options.

Investors will likely want a say on the token’s value accrual mechanism. This is because investors’ exit value will be defined by the token’s price (which is itself meaningfully influenced by the token’s value accrual mechanism). This is relevant because sometimes founders and investors have different views on value accrual (they have differing exit timelines and motivations). Investors can use their “say” in good ways and bad ways: for example, investors can use governance rights to push for more revenue sharing with token holders (which may potentially be perceived as “good” for the token price and from which they also directly benefit as tokenholders); on the other hand, they can also weaponize it to push for aggressively short token lock-in periods, or the ability to stake the investors’ locked tokens (both are generally perceived as “bad” for the token price).

Key Governance Terms

Since governance is a very important issue with broad and ripple-like impacts on a project and its stakeholders, it merits a deeper analysis.

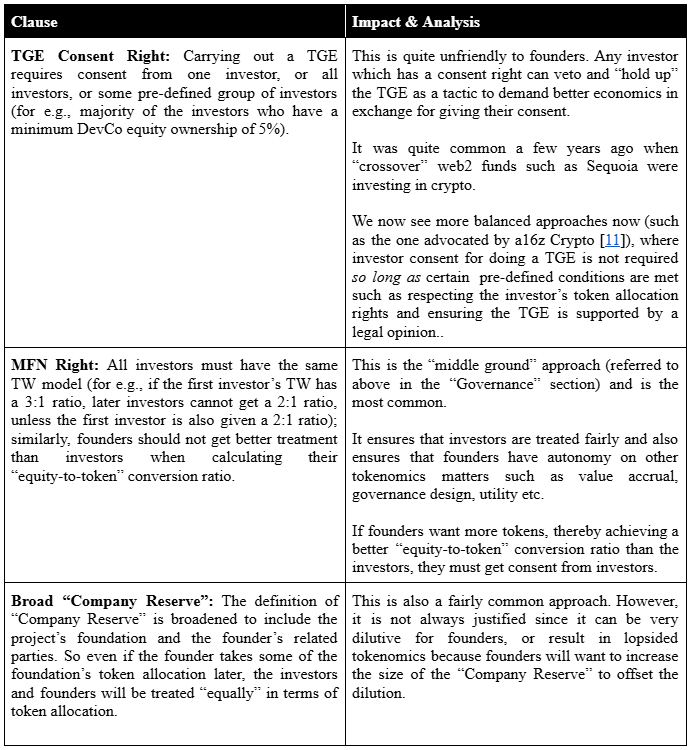

These are the typical governance terms of the TW:

As you can see, the governance terms of the TW need to be carefully structured and negotiated.

Consider a TW clause providing that the “Company Reserve” must be between 30% and 50% of the TNT, and that the final number will be decided by the DevCo’s board with the consent of the top 2 investors (by DevCo equity shareholding %). This might initially seem like a good idea because it gives flexibility to finalize tokenomics at a later date, instead of “freezing” the insider allocation prematurely at the seed/pre-seed stage. However, this practically has the same legal effect as giving these 2 investors blocking rights over the TGE, because the TGE cannot happen unless the tokenomics are finalized, and the tokenomics cannot be finalized unless the founder and these 2 investors agree on the size of the “Company Reserve”. Creative drafting is required to cure these second order effects of consent rights.

The MFN right should include targeted carve-outs so that more favourable token allocations can be given to strategics (for example, it might be appropriate for CEX venture arms to get more favorable ratios than other investors, if they are enabling a CEX listing).

Using the “Company Reserve” model gives the investor group more control/visibility over the maximum extent of the insider allocation than they would have if the investors only have an MFN right in their TW (i.e., if founders want to increase the insider allocation, investor’s permission is required).

Once a project starts using a TW model, the same model is usually used across its subsequent funding rounds. It is difficult for founders to renegotiate and convince investors to use a different model. However, such a “reset” of investor token allocations may well be required. The reset is easier if the TW provides that token allocation of investors can be revised with the consent of a super-majority of the investors (similar to the YC SAFE), so long as none of the investors are singled out for disproportionate treatment. Such terms are rare and VCs typically will not agree to such terms.

Conclusion

Here are some broad points to help investors & founders approach TW negotiations.

To draw a parallel with web2, early stage investors deploy less capital and only seek to safeguard their own economics (speed is critical in 0-1), but late stage investors deploy more capital and also seek to put in place robust governance mechanisms as the project matures (due to higher $ investment, survival and sustainable growth matters more). Crypto VCs should follow this principle and ensure that (at pre-seed/seed) their governance asks are targeted, minimal and flexible, not heavy-handed and prescriptive playbooks.

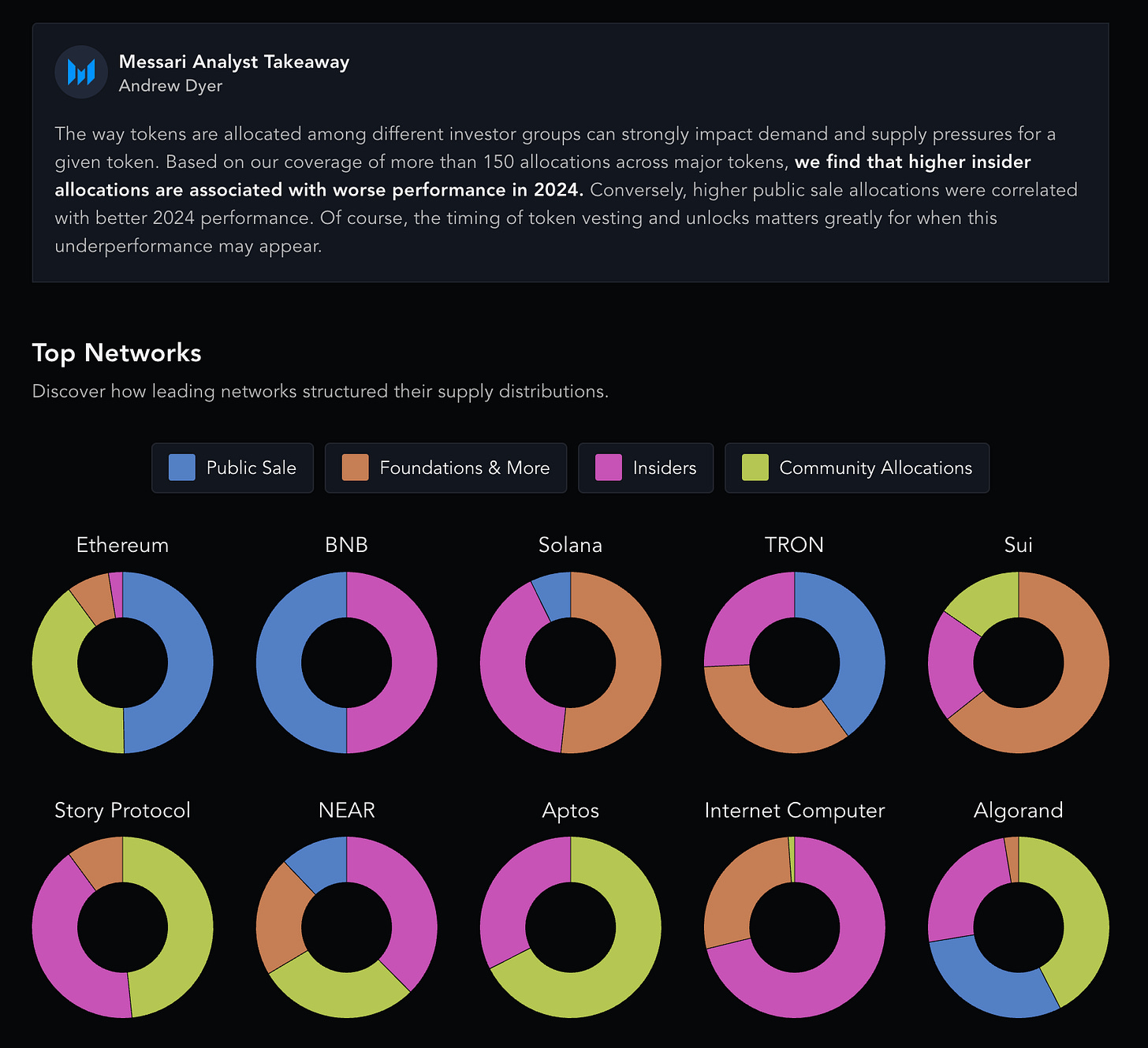

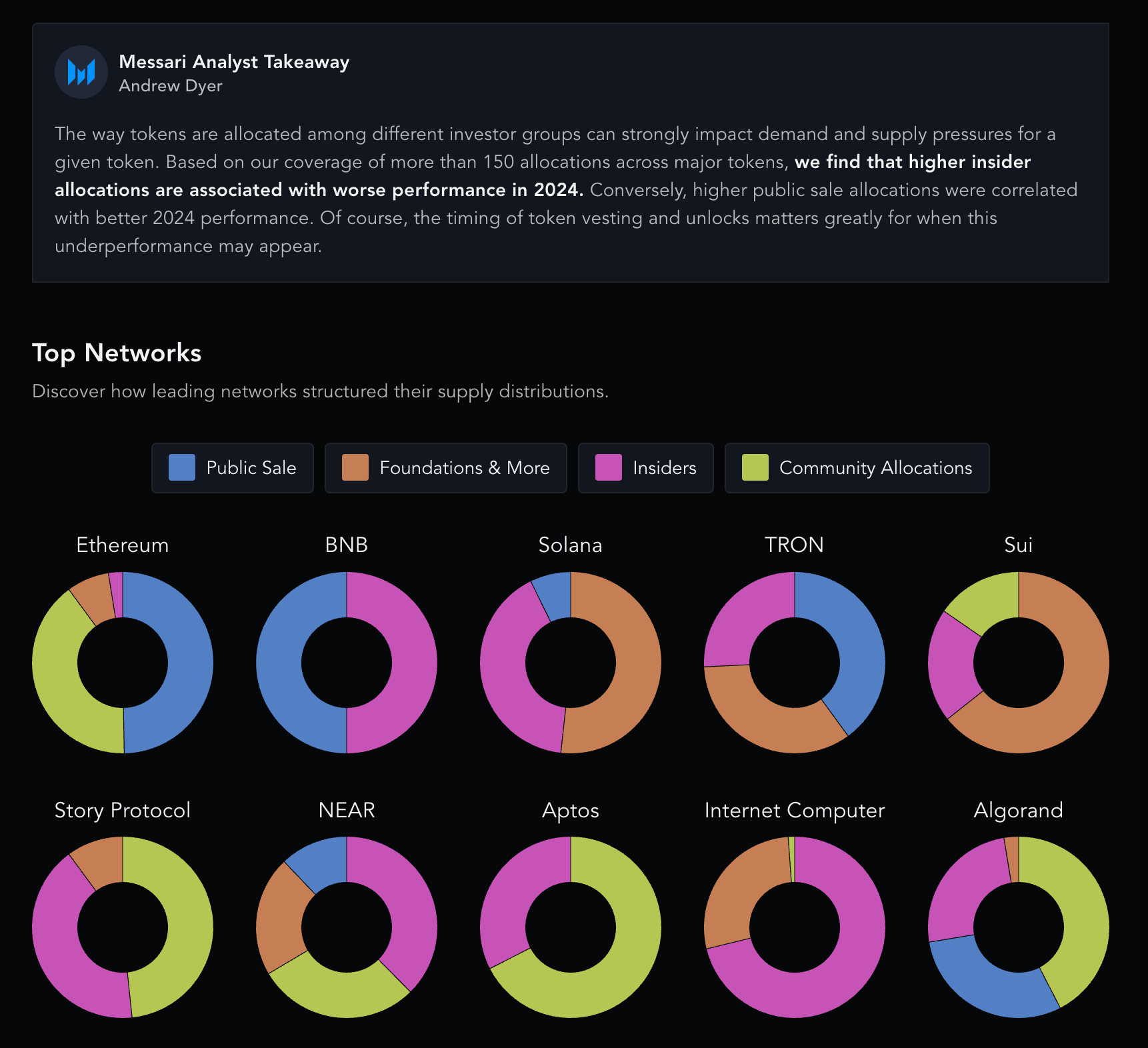

From an investor perspective, investors should be thoughtful about asking for very investor friendly terms, like a “Fixed Percentage” model or a 1:1 ratio. Why? As soon as one investor gets it, it becomes a template and others demand it too - resulting in lopsided tokenomics, or a governance structure where every investor has a veto over the TGE - these are lose-lose outcomes. Investors should also be open to clauses that allow a reset of investor token allocations. The reason why investors should be open to this: founder friendly terms usually enable the founder to structure more sustainable tokenomics that can help the project grow strongly post TGE, which in turn benefits the investors at the right time (i.e., when their tokens are eventually unlocked). This is supported by recent Messari research - see below12.

The best TW model for founders is a variant of the “Company Reserve” model where the “Company Reserve” is not fixed up front, but can be decided by founders later on. Investors can and will build in protections around this construct (like a range, a floor, or a cap), but this approach (i) sufficiently aligns incentives across the board, and (ii) ensures both sides have some clarity on the FDV of the deal, if the range is sufficiently small. Founders should also push for the ability to reset investor token allocations as long as a majority of investors consent.

To conclude, while deal structures like SAFE + Token Warrant and SAFT are often perceived as ‘simple’ or ‘standard’ they require founders to make very project-specific decisions around capital, governance and tokenomics. TWs should therefore be structured & drafted with a lot of commercial sensitivity, since the choices made in the TW can shape the trajectory of a project. Because “the big print giveth, and the small print taketh away”, founders should do two things: (i) make sure the VCs they are partnering with do not have a bad reputation (especially for predatory deal terms), and (ii) lawyer up anyway (expecting predatory deal terms).

On the tech side, founders can now also benefit from onchain flavors of SAFE + TW & SAFTs such as MetaleX’s cyberRaise13 which offers functionalities like escrows and simultaneous signing & funding. The crypto market is accelerating, so we expect the deal terms described above to coalesce around an industry “standard” to match this need for speed.

https://saftproject.com/static/SAFT-Project-Whitepaper.pdf

https://saftproject.com/

https://filecoin.io/blog/posts/token-sale-completed/

https://coinlist.co/assets/index/filecoin_2017_index/Filecoin-Sale-Economics-e3f703f8cd5f644aecd7ae3860ce932064ce014dd60de115d67ff1e9047ffa8e.pdf?

https://coinlist.co/assets/index/filecoin_2017_index/Protocol%20Labs%20-%20SAFT%20for%20Filecoin%20Token%20Presale-0f43e05c4ad1c0bd8993b60c4d6bf3cbd4f3d278dd7a62dde1972c9d82c65184.pdf

https://law.justia.com/cases/federal/district-courts/new-york/nysdce/1:2019cv09439/524448/227/?

https://www.goodwinlaw.com/en/insights/blogs/2020/04/sec-wins-injunctive-relief-to-prevent-telegrams-di?

https://www.theblock.co/post/171609/why-equity-plus-token-warrants-is-the-new-go-to-formula-for-crypto-vcs?

https://www.lattice.fund/writing-and-press/2022-seed-stage-retrospective

https://a16zcrypto.com/posts/article/token-rights-in-term-sheets-how-to-avoid-predatory-deals/

https://a16zcrypto.com/posts/article/token-rights-in-term-sheets-how-to-avoid-predatory-deals/

https://messari.io/token-unlocks/allocation-analysis?destination=token_unlocks

https://cybercorps.metalex.tech

| A guest post by

|

| A guest post by

|

Thanks for this insightful 🙂 article