SAFE + Token Warrant: Understanding the Meta, Part 1

SAFE & Token Warrants define early-stage crypto VC. This blog explains the SAFE's drawbacks & trade-offs, and shares our insights based on the crypto VC market to help founders effectively use SAFEs.

Introduction

Crypto projects broadly have two fundraising avenues: equity fundraise and token sales. At the pre-seed/seed stage (and sometimes even beyond) a combination of Y Combinator’s SAFE1 and a “token warrant” has become the preferred deal structure for crypto VC deals.

However, the SAFE & token warrant structure has traps for the uninitiated. This blog post aims to share our insights on the SAFE from a crypto deal context. Part 2 of this blog post will analyze the token warrant & SAFTs.

Market Context

Last year’s funding scoreboard: USD 19.6B was raised across ~3,500 crypto VC deals in 20242, so deal activity rebounded from 2023 levels3.

Most of the crypto VC activity in 2024 was concentrated at the earliest stages45, though later-stage deals were more prominent in Q1 FY25 indicating a maturing sector6.

In the US, almost all pre-seed and seed stage crypto deals utilized the SAFE7.

The crypto VC market has some notable features:

Since most deals are early stage deals the pace of dealmaking is frenetic. Anyone on the “Crypto Fundraising” Telegram channel can see the high volume of deals8. Relative to later stage investors, pre-seed and seed investors do not carry out extensive diligence and typically commit quickly. The market has become crowded.

Often, there is a speculative premium built into crypto VC valuations reflecting the frontier nature of the tech and undiscovered TAM. Galaxy Ventures says 2024 had a “particularly competitive environment that favored founders in their valuation negotiations”. Their data demonstrated that despite the higher risk relative to TradFi VC, crypto VC opportunities are being bid up9.

Many crypto VC rounds are party rounds with a variety of investor personas: VC funds (which includes “leads” and “follow-ons”), strategic angels, KOLs, advisors, family offices, crypto ecosystems, accelerators, ‘anon whales’ contributors and strategics.

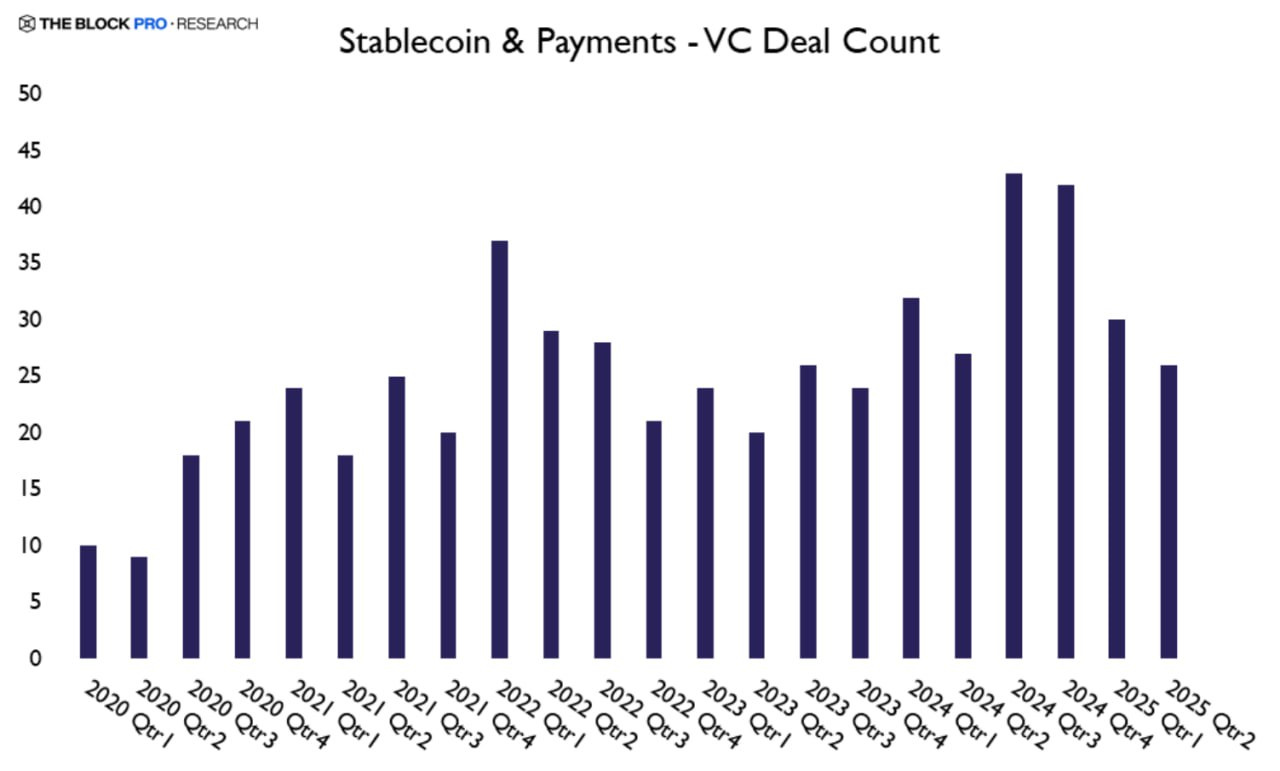

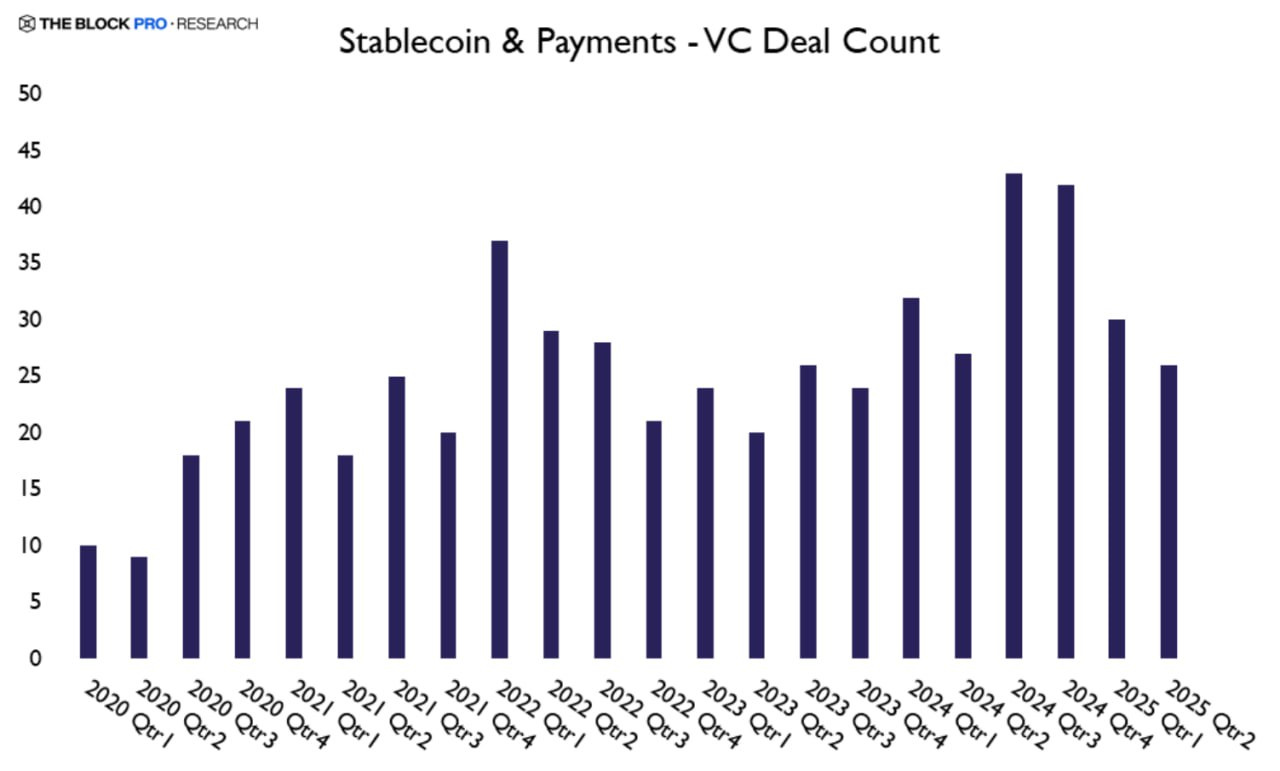

Positive developments on the US regulatory side, the snowballing pace of stablecoin adoption, the generational “pop” of Circle’s shares post listing, and the emergence of the first few “big bang” crypto M&A deals are tailwinds for the crypto VC market. The quarterly capital invested was the highest since Q3 FY2210. There is already a noticeable spike in deals in the stablecoin & payments space. This implies that the crypto VC market will not only continue to thrive, but heat up considerably in 202511.

To summarize, this is a high-velocity market where investors need to do deals fast and live with valuation asks on the higher side, while founders need to create FOMO and “herd cats” to close quickly from a diverse investor set between turbulent market cycles and metas.

These conditions make the SAFE the ideal investment structure for the current crypto VC market, but dealmakers should understand the SAFE’s nuances.

Round & Pricing Dynamics

The SAFE is a short and simple (yet deceptively complicated) funding agreement.

The key commercial implications of SAFEs are:

SAFEs are standardized and they have zero in-built governance terms, so there is minimal legal negotiation, resulting in a very smooth and fast dealmaking process.

Using SAFEs, founders can do a “rolling close” where they collect money from a pipeline of investors over a 2 or 3 month period. This is in contrast to a “priced round” where the founder has to wait until all the various investors in their funnel get confirmed and then “close” the confirmed investors simultaneously at the end of the fundraising journey (Y Combinator explains this by invoking Paul Graham’s seminal “high resolution fundraising” blog post12).

The investor’s stake is not fixed at the time of investment based on the project’s valuation. Instead it is linked to the project’s future valuation in its first “priced” round (it can be a pre-series A, a series A, or even a down round compared to the SAFE’s valuation cap).

Let’s spend more time on point #3 since it is important. How is the investor’s stake “linked” to the project’s future valuation? Through the SAFE’s “valuation cap”, which works like this: if the priced round’s valuation is above the valuation cap then the investor’s stake is computed using the valuation cap as the post-money valuation; if the priced round’s valuation is below the valuation cap then the investor’s stake is computed using the series A pre-money valuation. See this illustration:

In a SAFE deal investors underwrite the project’s valuation at the first “priced” round after the SAFE investment. An investor using a SAFE with a USD 20M valuation cap is effectively saying: “Your valuation may not be USD 20M right now, but as long as another investor prices you at USD 20M in a future round then I am okay to give you a valuation of USD 20M at this moment in time too”. In theory, this is extremely founder friendly.

In practice, it would be too good to be true if an investor’s offer was: “I’ll fund you now and take the risk now but my entry valuation will be fixed later on when you have scaled to a point where other investors show conviction”. Since the SAFE’s valuation cap effectively gives an investor a guaranteed “base case” shareholding, investors and founders negotiate the investor’s “base case” shareholding and in doing so, effectively negotiate a valuation.

TL;DR: the valuation cap is the valuation in a SAFE deal unless the project’s next “priced” fundraise is a down round. It is a myth that SAFE rounds are “unpriced”.

SAFE’s Drawbacks & Trade-Offs

SAFEs have received plenty of justified criticism. That said, we believe that the SAFE’s drawbacks are accepted as a trade-off to get the benefits of the SAFE.

1. Increased Dilution vs. Deal Closing Flexibility

2. Full-Ratchet Anti-Dilution vs. Increased Valuation

Our Insights

Excessive Dilution: SAFEs lead to excessive dilution when projects do multiple rounds of SAFE funding. The dilution is amplified if subsequent SAFE rounds are large in size. Ideally, projects should raise as little as possible on SAFEs and do the “priced” round as soon as possible. The data clearly shows that this is the preferred route15.

Exception in Crypto VC: That said, in crypto VC there have been large rounds at high valuations using SAFEs (for example, QED’s USD 6M round - at an allegedly >USD 100M valuation - led by Blockchain Capital16).

What are the reasons for this trend, which we find repeatedly in the crypto VC space?> In crypto VC deals the investor’s equity stake and share of tokens is correlated through the “equity-to-token” ratio (and the investor’s right to get tokens is captured in the token warrant). If (i) it is clear that the ultimate exit/value accrual for that project is through tokens and (ii) this ratio is high (for e.g. 3:1 or 4:1), then it’s okay to take more equity dilution by using a SAFE because token dilution is minimized. In such cases it may make sense for founders to do a faster SAFE deal to quickly capture the favorable deal terms (and this comes with the added advantage of low/zero governance rights for investors).

> It is possible that crypto founders are okay with slightly more dilution at the early stages since funding post TGE is non-dilutive to founders (i.e., funding post TGE happens through sales from the project’s treasury and often at very mature valuations - an example is Polygon’s USD 450M private token sale in 2022, led by Sequoia Capital India).

“Bridge Round” Exception: If a project quickly needs a small amount of bridge capital to meet the milestones necessary for a bigger, more impactful series A round in the near future, it could make more sense to do a small SAFE round since they significantly minimize the negotiations around a typical “priced” round. This is just a way of saying that velocity matters at the seed & pre-seed stages so as an exception to #1, founders should not optimize for conserving equity if it makes more sense to get money in the bank fast and continue building.

“Acceleration Mode” Exception: To caveat #1 again, “get the money in the bank fast” is a very important operational principle for dealmakers. Stephen Schwarzmann’s autobiography repeatedly calls out that “time wounds all deals”. If the market is extra volatile (for example, in the aftermath of Terra/Luna or FTX) or if the strongest possible social proof signal can be sent by closing a SAFE round with a Tier 1 VC immediately (which then paves the way for quickly closing the rest of the round) then it makes sense to use a SAFE instead of risking a long-drawn out negotiation over “priced” round transaction documents with multiple counterparties.

Modeling Dilution: Because of the embedded “full ratchet” anti-dilution it’s important for founders to model dilution from SAFEs like this: “My base case shareholding is X% after the first SAFE round, but if the next round happens at a USD Y valuation then in a worst case my stake could go down to Z%”. This kind of modeling is especially required when significant amounts are being raised at aggressively high valuations in bull markets. To quote Mark Suster again: “full-ratchet anti-dilution is a nuclear option; it socializes upside and privatizes downside”.

Option Pool Shuffle: If an option pool is created around the time of a SAFE round (the SAFE’s language leaves the exact timing unclear) it is dilutive for founders but not SAFE investors. If an option pool is created just before the closing of the series A round - which is what series A investors will insist on - then it will dilute both the founders and the SAFE investors. This means that founders are incentivized to create bigger option pools just before the series A so that they share dilution from the option pool with the SAFE investors.

Use Every “Option”: A related issue cannot be better explained than through this screenshot below17.

Along with point #6 above (Option Pool Shuffle), the implication is that founders should carefully plan their “budget” of stock options along with the hiring & funding roadmap. We recommend tools like Carta or Pulley (or even Google Sheets) to manage and model cap tables.

No Governance Terms: The lack of governance terms in SAFE deals becomes an issue when one co-founder decides to quit or starts spending time on another project - that co-founder’s equity becomes deadweight but (typically) no one has the ability to claw the deadweight equity back and use it to incentivize a new co-founder. This is not just an investor problem of course - it’s a problem for the other co-founder(s) too! Ideally, co-founder agreements and/or governance side letters should be put in place to address this. The market clearly recognizes the lack of governance terms in SAFE deals because SAFEs become less common as the round size goes up18.

MFN Rights: It is common for lead/significant investors to ask for an MFN right on SAFE terms in the very first SAFE round. For subsequent SAFE rounds (if the commercial circumstances permit) founders should push for limiting or removing all MFN rights. MFNs can have a domino effect of dilution if the subsequent SAFE rounds have lower valuation caps than the initial SAFE rounds. Such volatility in valuations can occur when the market oscillates between bear & bull markets quickly, or when there are unforeseeable regulatory headwinds (these are unfortunately the defining characteristics of the crypto market).

Discounts: It is possible to build a discount into a SAFE’s valuation cap (for example, if the project’s next round is at USD 30M, and the SAFE has a 10% discount, then the SAFE investor’s effective entry valuation is USD 27M). This discount feature should be used very sparingly to lure high-quality lead investors to commit first. However, as the below screenshot illustrates, this is a tricky balancing act19. It can be difficult to tell the investment committee of institutional follow-on investors that they need to come in at a higher price in the same round unless a convincing narrative exists for the disparity.

Conclusion

We acknowledge that we have significantly complicated what was intended to be a very simple investment agreement but it is important to understand this complexity, especially when it is correlated to tokenomics.

We believe that the SAFE will remain the gold standard for crypto VC deals, especially due to innovations in tokenizing the SAFE and adding crypto guardrails - the most notable ones being MetaLex’s cyberSAFE20 and LexTek’s SAFE NFT21 (by Gabriel Shapiro and Ross Campbell respectively).

Please read Part 2 of this blog post (coming soon™), which will discuss fundraising via SAFEs + token warrants & SAFTs.

Disclaimer: This post is for informational purposes only and does not constitute legal, financial, or investment advice.

https://www.ycombinator.com/documents

https://outlierventures.io/article/2024-in-review-fundraising-in-web3/

https://www.galaxy.com/insights/research/crypto-blockchain-venture-capital-q4-2024

https://outlierventures.io/article/2024-in-review-fundraising-in-web3/

https://www.galaxy.com/insights/research/crypto-blockchain-venture-capital-q4-2024

https://www.galaxy.com/insights/research/crypto-venture-capital-q1-2025

https://carta.com/data/state-of-pre-seed-2024

https://t.me/crypto_fundraising

https://www.galaxy.com/insights/research/crypto-blockchain-venture-capital-q4-2024

https://www.galaxy.com/insights/research/crypto-venture-capital-q1-2025

https://www.dlnews.com/articles/deals/experts-predict-what-to-look-for-in-crypto-vc-trends-in-2025/

To illustrate, consider this example: Total number of shares in company: 75,000; lead investors 's shareholding: 5,000 shares; lead investor's shareholding percentage: 6.6%.

Two months after the lead closes, if the company closes a group of strategic angels, who buy 3,000 shares, then: the total number of shares in the company becomes 78,000 and lead investors's shareholding percentage becomes 6.4%.

https://bothsidesofthetable.com/the-truth-about-convertible-debt-at-startups-and-the-hidden-terms-you-didn-t-understand-9fccf6854dee

https://www.linkedin.com/posts/peterjameswalker_startups-safes-valuationcaps-activity-7331008687643299841-M2Rn/

https://www.theblock.co/post/303375/bitcoin-scaling-protocol-qed-funding-valuation

https://www.linkedin.com/posts/joshephraim_if-youre-raising-capital-via-ycs-post-money-activity-7329215412372492290-zoXI/

https://carta.com/data/state-of-pre-seed-2024/

https://x.com/sajithpai/status/1537398220204429312

https://cybercorps.metalex.tech/

https://safe.lextek.eth.limo/

| A guest post by

|

| A guest post by

|