Unpacking the Stablecoin Value Chain: Who Enables, Who Profits, and Who Pays.

Behind the global stablecoin adoption lies a value chain comprising of different players. This article unpacks who they are and the distinct roles they play in powering the stablecoin ecosystem.

Introduction

Stablecoins have become one of the most consequential innovations in digital finance, powering billions of dollars in transactions, bridging the gap between crypto and traditional banking system, and promising faster, borderless payments. From 2020 to 2025, the stablecoin market experienced exponential growth. Total supply expanded from $5.9 billion in early 2020 to over $308 billion by Oct 2025, marking over 38x increase over five years, which was fuelled by the DeFi boom of 2021, retail usage for remittance and cross-border payments and expanding institutional participation.

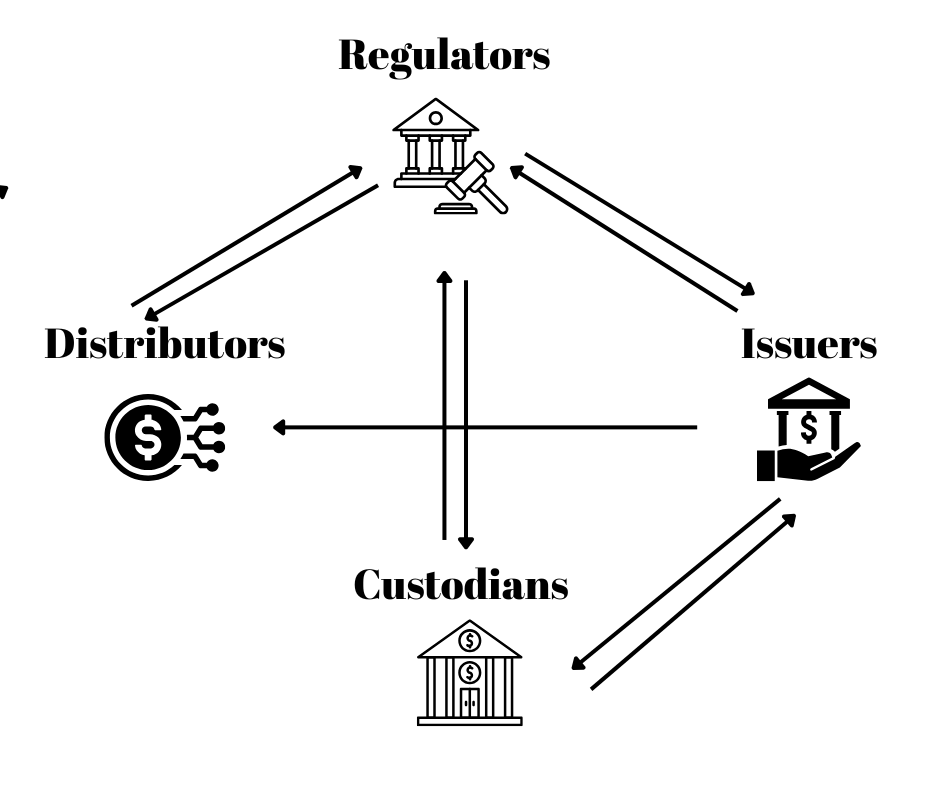

Yet behind this rapid adoption lies a complex value chain of actors - issuers, custodians, market makers, exchanges, on and off ramp platforms, regulators, and end users, each playing a distinct role.

Regulators sit at the top of the stablecoin value chain, setting the rules for how these assets can be issued, backed, and circulated. As adoption accelerates, they are racing to catch up, introducing policies to mitigate risks and protect consumers. Issuers like Tether and Circle anchor the system by creating billions in digital dollars and managing the reserves behind them, while custodians safeguard those reserves and ensure compliance.

Distributors like exchanges and wallets fuel liquidity. Fintech companies such as PayPal and Stripe are also beginning to integrate stablecoin into their payment offerings, expanding access and distribution to millions of users globally. At the end of the spectrum, end users particularly in emerging markets, are increasingly using stablecoin for remittances, savings, and cross border payments offering a more stable alternative to their local inflationary currencies and unreliable banking systems.

As stablecoin become more deeply embedded in both decentralised finance (DeFi) and traditional payment systems, it’s increasingly important to understand the dynamics beneath the surface to examine who actually benefits, who assumes the risks, and how value is distributed.

This article unpacks the stablecoin value chain to answer the question: in this growing financial architecture, who enables it, who pays, and how does value flow across participants in the value chain?.

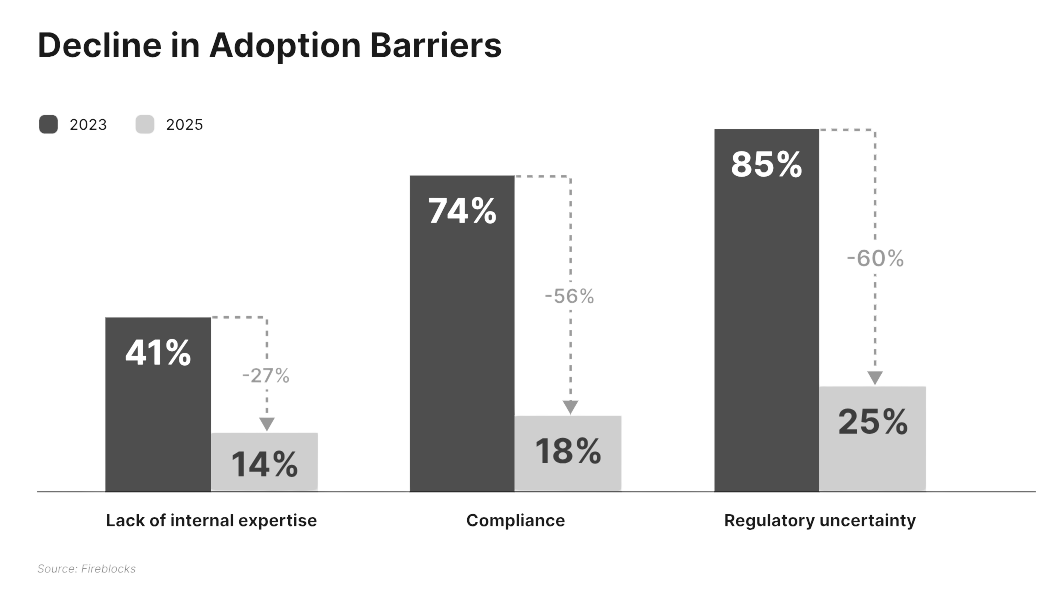

Regulatory costs shape stablecoin economics and raise entry barriers

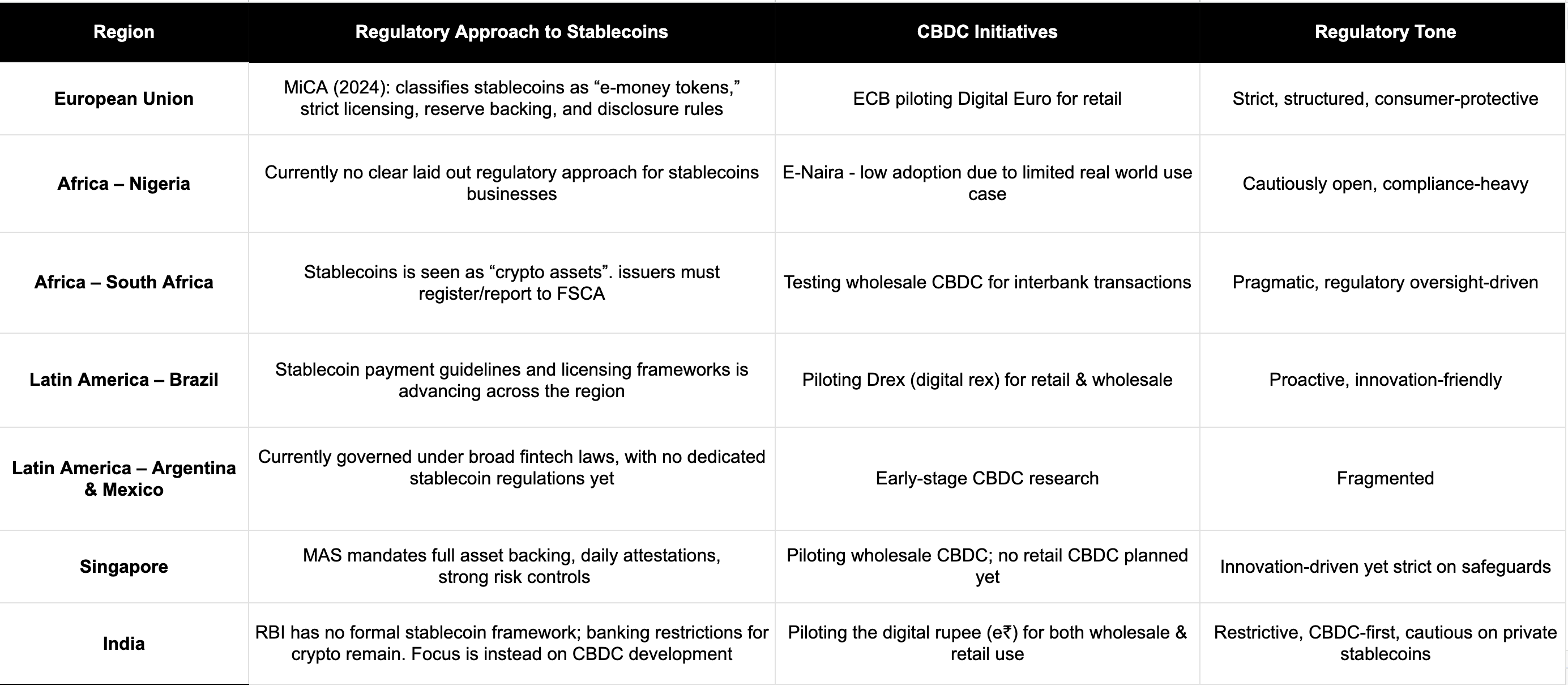

Stablecoin regulations are the foundational framework upon which every other player in the value chain operates. It is the decisive force shaping the stablecoin value chain. Each major region around the world is taking a distinct approach to regulate both private stablecoins and central bank digital currencies (CBDCs) as regulatory uncertainty is now gradually giving way to clearer, and more defined frameworks.

The European Union’s MiCA regulation, effective since 2024, classifies stablecoins as “e-money tokens” and enforces strict licensing, reserve backing, and disclosure requirements for issuers operating in the region. In parallel, the European Central Bank is piloting a digital euro, emphasising privacy and practical use for retail usability.

In Africa, regulatory attitudes are evolving: Nigeria although unclear regulatory approach particularly towards stablecoin platforms has shifted its stance on crypto, even as USD stablecoin adoption continues to grow. Kenya recently passed the VASP bill into law, creating an even stable regulatory environment for stablecoin platforms. South Africa, with the most advanced regulatory environment in Africa treats stablecoin as “crypto assets” and enforces registration and reporting through the Financial Sector Conduct Authority, while testing a wholesale CBDC for interbank use.

Latin America presents a patchwork of regulatory approaches: Brazil is leading in the region with stablecoin payment guidelines and a developing licensing regime, alongside pilot trials of its Drex (digital real) for retail and wholesale use. In contrast, Argentina and Mexico rely on broader fintech laws to govern stablecoin activity, while both explore early-stage CBDC research.

Singapore has also emerged as a global leader in digital asset regulation, with the Monetary Authority of Singapore (MAS) requiring stablecoin issuers to maintain full asset backing, daily attestations, and robust risk controls. While it is piloting a wholesale CBDC for interbank use, Singapore has no plans for a retail version, highlighting its pragmatic and innovation-driven regulatory stance.

India has taken a cautious approach, with the Reserve Bank of India (RBI) yet to establish a formal regulatory framework for stablecoins and maintaining restrictions on crypto-fiat banking. Instead, the country is prioritising its own CBDC, the digital rupee (e₹), now in pilot for both wholesale and retail use, aiming to reduce dependence on private stablecoins for domestic and cross-border transactions.

The GENIUS Act, signed into law on July 18, 2025, by President Donald J. Trump, marks America’s first comprehensive stablecoin legislation. By setting clear regulatory standards that emphasize consumer protection and transparency, the Act strengthens the dollar’s dominance in the digital asset space and positions USD-backed stablecoins as the default medium for cross-border digital transactions. For emerging markets, this framework presents both opportunities and risks: it could enhance trust and credibility in stablecoin adoption, but it may also create access barriers that risk sidelining local players from participating fully in the global digital economy.

Genius Act and its Implications in Africa’s Emerging Market

The GENIUS Act framework in the USA is expected to have meaningful impacts on Emerging Markets such as Africa, with several implications:

Issuers stand to capture more significant value from Africa’s expanding stablecoin ecosystem, where confidence in U.S.-regulated stablecoins is boosting their use in remittances, trade, and cross-border payments.

However, the GENIUS Act places strict conditions on foreign stablecoin issuers seeking access to the U.S. market, including compliance with U.S. regulatory standards and the requirement to maintain reserves in U.S. institutions. This could limit the ability of issuers from emerging markets and other regions to directly access and operate within the U.S. stablecoin market

The framework is also expected to inspire the adoption of similar comprehensive stablecoin regulations across African countries, in the bid to promote safer markets and stronger consumer protections.

Global Outlook: Regulatory clarity is becoming a key enabler of institutional participation, while ambiguous or restrictive rules risk stalling innovation and pushing activity into gray markets. It has also become the catalyst for a more competitive stablecoin ecosystem, attracting a growing number of new issuers.

Another effect of regulatory clarity is on CBDCs. Although their adoption and development remains uneven and relatively low across most regions, they are largely being developed to complement stablecoins, particularly in retail and interbank payments.

Stablecoin issuers makes revenue from minting, redemption, and float management

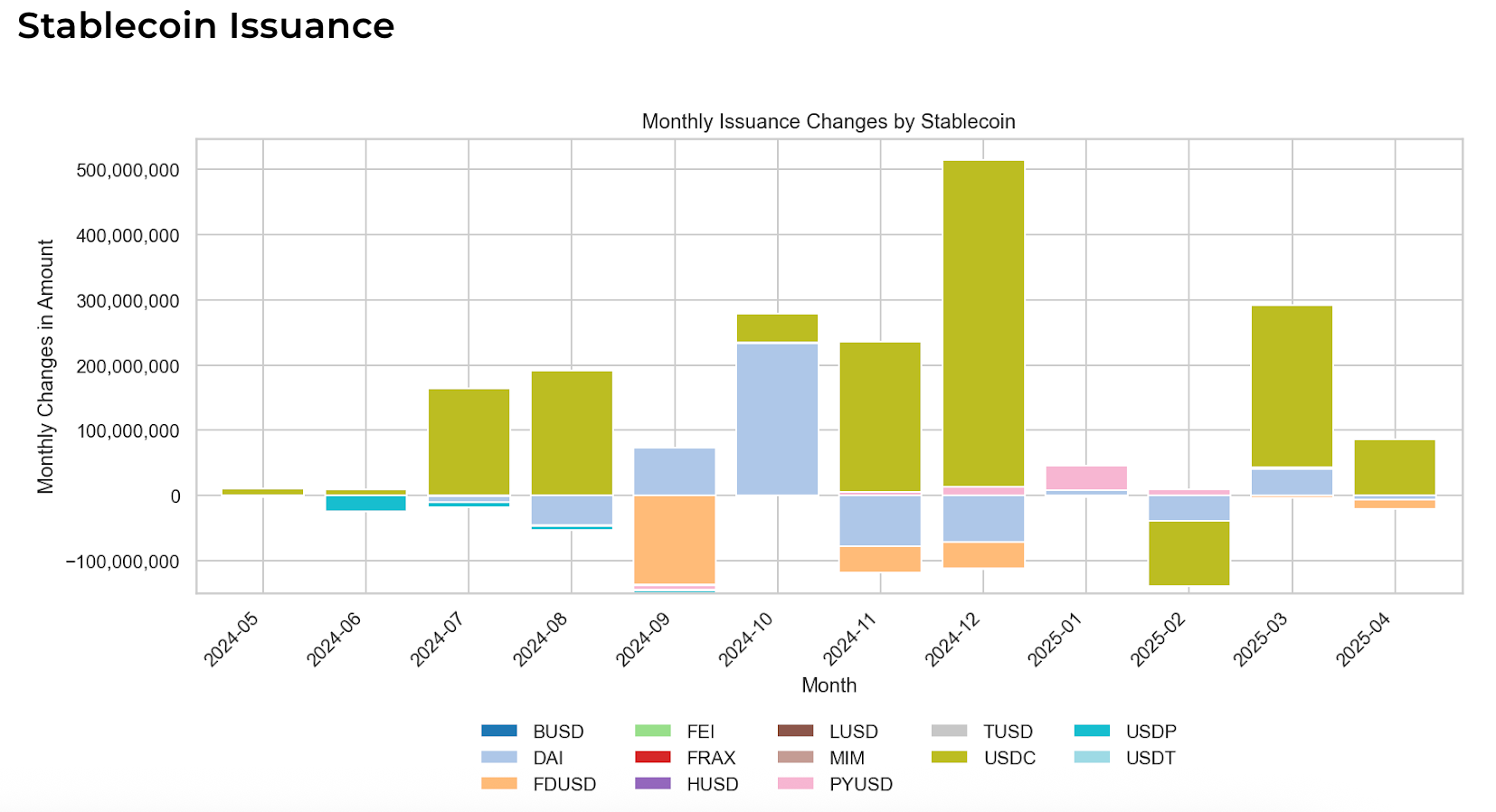

Stablecoin issuers like Tether (USDT) and Circle (USDC) have evolved into financial powerhouses, minting digital dollars at a scale with reserves that rivals foreign exchange reserves of some countries. Between 2024–2025, Tether’s circulating supply surpassed $180 billion, with Circle’s USDC also surpassing $75 billion after a temporary dip in 2023. These private entities now manage dollar-denominated instruments with monetary influence greater than that of many central banks and national economies. Combined, these two giants now account for more than 90% of global stablecoin volume, with year-over-year growth rates of 30–50% as demand accelerates in both developed and emerging markets.

However, this dominance is unlikely to remain unchallenged. New entrants are actively reshaping the stablecoin landscape. For example MetaMask recently launched MetaMask USD ($mUSD), becoming the first self-custodial wallet to issue its own stablecoin, tightly integrated into its ecosystem of swaps, bridging, and payments. At the same time, other stablecoins like Ethena’s USDe and new players like Phantom’s $CASH have rapidly expanded supply. As of August, 2025, USDe’s circulating supply reached $12 billion while $CASH reached $73million since it’s launch in September 2025. Other web3 projects, large fintech players are increasingly exploring custom stablecoin solutions These developments suggest a more fragmented and competitive stablecoin market ahead, with implications for both market share structure and adoption.

How Stablecoin Issuers make money:

Investing reserves (primary revenue engine)

In the stablecoin ecosystem, the term “float” refers to the pool of fiat currency, typically U.S. dollars that users deposit in exchange for stablecoin. While users receive the stablecoin for use in payments, trading, or savings, the actual fiat remains with the issuer. This “reserve capital”, “or float”, is then invested by issuers like Tether and Circle in low-risk, interest-bearing assets such as short-term U.S. Treasuries, reverse repos, and money market funds. Because the issuers retain control over these funds, they earn interest on them and with interest rates at multi-year highs, this float has become a major profit engine, allowing issuers to generate billions in revenue: Tether reported over $4 billion in profit in Q2 2025 alone, driven by $120 billion in Treasury holdings. While Circle reported a $658 million in reserve income, with over 90% in Treasuries and repos, and the remainder in cash at regulated banks.

Minting and redemption fees

Stablecoin issuers also generate revenue through minting and redemption fees, though these are relatively minor compared to the substantial income from reserve investments. As the market matures, transparency has become non-negotiable: both Tether and Circle now publish attestation reports (Tether Q1 2025, Circle Transparency). In the U.S, the AICPA has introduced stricter disclosure guidelines for stablecoin issuers. Europe’s MiCA framework on the other hand is setting new standards around reserve transparency, redemption rights, and consumer protections.

Circle’s initial public offering (IPO) in June 2025 was a watershed moment for the digital assets industry. Trading on the NYSE under the ticker CRCL, Circle raised $1.1 billion and closed its debut day valued at roughly $18 billion. Investor enthusiasm on stablecoins quickly drove the stock to a peak of over $200 per share, pushing Circle’s market capitalization to above $70 billion. Since that peak, Circle’s stock has seen a sharp correction. As of September 2025, CRCL trades at about $144 per share, giving the company a market capitalization of roughly $33 billion. The decline shows that even as adoption continues, sentiments are still volatile.

Treasury operations maximize reserve returns while managing risk and liquidity

The heart of the stablecoin business for issuers is treasury management. While minting fees provide some revenue, the real engine is the yield generated from investing reserves. Tether’s Q1 2025 attestation report revealed that 81.5% of its reserves were in cash, cash equivalents, and short-term deposits, mainly U.S. Treasuries. Circle’s February 2025 report showed a similar tilt, with nearly all reserves in Treasuries, repos, and cash.

But yield comes with risk. Issuers must balance maximizing returns with maintaining instant redemption liquidity. Circle, for example, keeps a higher proportion of cash and overnight Treasuries to enable real-time redemptions, while Tether maintains substantial excess reserves, $5.6 billion as of Q1 2025, to cushion against market shocks.

In March 2023, the sudden collapse of Silicon Valley Bank (SVB) triggered one of the most dramatic episodes in stablecoin history, exposing the fragility of even the most trusted digital dollars. SVB, a key banking partner for the tech and crypto sectors, entered receivership after a $42 billion bank run, with Circle revealing that $3.3 billion of its reserves were trapped at SVB, about 8% of all USDC backing at the time. This disclosure caused panic across crypto markets, and USDC, typically pegged 1:1 to the U.S. dollar, rapidly depegged, plunging to $0.8789 on March 11, 2023.

The crisis led to a net outflow of nearly $4 billion in USDC supply within days, as holders rushed to redeem or swap their tokens for other assets. The depeg also rippled through the stablecoin sector, with alternatives like DAI and TUSD seeing significant inflows as users sought safety.

US regulators intervened, guaranteeing SVB deposits and restoring confidence. USDC quickly regained its peg, but the episode underscored the importance of transparent reserve management and robust risk controls for stablecoin issuers.

Custodians monitize their role as trusted asset holders

Custody is where the value chain’s trust is forged. After the collapse of companies like FTX and Celsius, it’s now standard for stablecoin projects to keep customer funds legally separate, protect them in case of bankruptcy, and provide frequent, transparent audits to prove the money is really there.

These custodian banks where reserves are kept serve as the critical bridge between reserves and regulation, quietly monetizing the float while enabling scale. Two major role they play in managing stablecoin reserves, is providing security and regulatory oversight. Their role is pivotal as without trusted custody, neither institutional nor retail users would have confidence in the 1:1 backing of stablecoins.

How do custodians make money? Their model is simple but powerful: charge 0.1–0.5% of assets under custody (AUC) annually. They earn these fees for holding and managing stablecoin reserves, while providing security and regulatory oversight. Example, with Coinbase custody alone holding $101 billion in AUC as of 2025, the revenue potential is enormous. Custodians also differentiate through added services like staking, DeFi integrations, insurance, and SOC audits.

Some custodians and their assets under custody (AUC):

BNY Mellon: As circle’s primary custodian, BNY Mellon manages a significant portion of USDC’s reserves, supporting Circle’s transparency and institutional credibility. BNY Mellon’s overall digital asset custody business has grown rapidly, with total digital AUC exceeding $50 billion by mid-2025.

BitGo: BitGo is another major player, with $100 billion in digital assets under custody as of mid 2025. BitGo is known for its multi-signature wallets, insurance coverage, and integrations with DeFi and institutional trading platforms.

Anchorage Digital: Anchorage is a federally chartered crypto bank in the U.S., providing custody for stablecoins and other digital assets. By 2025, Anchorage’s AUC surpassed $50 billion, with a focus on compliance and institutional-grade security.

Fidelity Digital Assets: Fidelity’s crypto custody arm, targeting institutional investors, has reached over $20 billion in AUC, with a growing focus on stablecoin and tokenized asset custody.

Zodia Custody (Standard Chartered): Zodia, backed by Standard Chartered, has become a significant player in the UK and Asia, with AUC exceeding $10 billion by 2025, focused on regulatory compliance and institutional onboarding.

Distribution partners like exchanges, wallets and fintechs earn from transaction fees and trading spreads

If issuers and custodians are the engine and chassis, distribution partners such as exchanges, wallets and fintechs are the wheels that put stablecoins on the road. Exchanges like Binance, Coinbase, and OKX, along with wallets such as MetaMask and Phantom, and consumer-facing fintechs like PayPal and Revolut are at the fore front of expanding access and distribution of stablecoins to millions of users globally. In emerging markets, where traditional banking infrastructure is limited or unstable, distribution partners play an especially critical role onboarding new users, driving utility, and building the trust needed for stablecoin adoption to scale. A clear example of this dynamic is the multibillion-dollar deal between coinbase and circle, which strengthened their partnership around USDC distribution and adoption.

Exchanges profit from trading fees and spreads on stablecoin pairs, often among their most liquid markets. Wallets and fintechs monetize through transaction fees (MetaMask: ~$0.02 per USDT/USDC transaction), remittance charges, and custody spreads (PayPal: 2.99%+ per crypto transaction).

Perpetual swaps are now the most actively traded derivatives in crypto, and the vast majority are denominated in stablecoins, especially USDT. Binance, the world’s largest exchange, leads the market here with USDT-denominated perpetual swaps driving record volumes. In 2025, Binance held 59% of all stablecoin balances across exchanges (about $31 billion), with cumulative inflows of $180 billion year-to-date.

Onramp and offramp providers are making stablecoins accessible and earning from transaction volumes

Onramp and offramp providers are the critical bridge between fiat currencies and stablecoins, and their importance is most pronounced in regions where traditional banking infrastructure is limited or unreliable. These platforms, global leaders like MoonPay, Ramp, and Transak, and regional specialists such as Onmeta (India) and Onboard (Africa), typically charge 0.5–2% per transaction, with revenues scaling directly with transaction volumes.

The need for robust onramp and offramp infrastructure is greatest in emerging markets, where stablecoins often serve as a better alternative for remittances, savings, and cross-border payments. In these regions, access to USD or euro-backed stablecoins provides individuals and businesses with a vital hedge against currency devaluation and inflation. But the real value of this access lies in how it changes financial behavior by enabling people to bypass the inefficiencies, high costs, and delays of legacy banking systems, stablecoins become more than just a store of value, they become a practical tool for daily financial activity.

Africa:

Africa has become a global leader in stablecoin adoption, with annual stablecoin transaction volumes expected to surpass $30 billion by 2026. Onramp/offramp providers like Onboard and Yellow Card have seen explosive growth, enabling users to move between local currencies and stablecoins for remittances, payroll, and commerce. The continent’s high mobile penetration and need for cross-border payments have also made seamless fiat-stablecoin conversion a necessity.

Latin America:

Latin America is now the fastest-growing stablecoin market globally. The region’s demand is driven by currency instability and capital controls, with platforms like Ramp and Binance’s P2P onramps facilitating billions in monthly volume. In 2024, Latin America accounted for more than 20% of global stablecoin flows, with Brazil, Argentina, and Mexico leading adoption.

Asia:

In India, onramp/offramp providers such as Onmeta and Transak have enabled millions to access stablecoins for remittances and digital commerce. India accounts for approximately 2% of global stablecoin flows, indicating notable activity.

Why Onramps/Offramps matter more in Emerging Markets

Banking gaps:

Millions of people across Africa, Latin America, and Southeast Asia remain underbanked or entirely outside the formal financial system. Onramps/offramps allow them to bypass local banking bottlenecks and directly access global digital assets.

Remittance flows:

The World Bank estimates that remittances to low- and middle-income countries exceeded $650 billion in 2024, with a growing share routed through stablecoins due to lower fees and faster settlement.

Capital controls & inflation protection:

Emerging countries face strict capital controls, currency devaluation, or hyperinflation. Local users increasingly rely on stablecoins as a store of value and a means of moving money across borders. Onramps enables them to convert their local fiat into stable digital dollars, offering a way to preserve wealth and hedge against Inflation.

Regulatory arbitrage:

Where capital controls on foreign currency access or inflation erode savings, users turn to stablecoins via local onramps to circumvent regulatory friction. This allows them to access USD-backed assets, preserve capital, and conduct international payments outside formal banking oversight.

Business model and value chain impact: Onramp/offramp providers differentiate themselves through liquidity depth, regulatory compliance, and seamless user experience. Their business model is reinforced by partnerships with banks, fintech apps, and payment networks, as well as robust KYC/AML compliance. As more users are onboarded into the ecosystem through on and off ramps, the value chain becomes more efficient, benefitting issuers, custodians, and distribution partners alike.

Emerging markets are unlocking unique value chain opportunities for local entrepreneurs and users

Emerging markets have become the most compelling market for stablecoins not only because of the scale of unmet financial needs, but also because their practical utility is far more pronounced than in developed economies.

In the U.S. and Europe, stablecoins are often seen as trading instruments. In contrast, in countries like Nigeria, India, Brazil, and across southeast Asia, stablecoins are solving foundational problems, offering a lifeline for remittances, savings, payroll, and inflation hedging where local financial systems are fragmented or unreliable.

The numbers underscore this opportunity. Africa alone processed over $20 billion in stablecoin transactions in 2024, with companies like Yellow Card reporting $3 billion in annual volume, and Juicyway processing $1.3 billion till date. In Latin America, platforms such as Belo (Argentina) and Bitso (Mexico/Brazil) are also leveraging stablecoins to help users hedge against currency devaluation and facilitate cross-border payments. India, Nigeria, and Indonesia consistently rank among the top countries for stablecoin usage, with Nigeria using stablecoins to hedge against currency devaluation and streamline cross-border flows.

Ultimately, the difference is stark: in developed markets, stablecoins are a convenience; in emerging markets, they are a necessity. The companies winning in these regions are those building for local context - integrating with mobile money, solving for FX volatility, and prioritizing regulatory compliance and user experience.

Africa’s dollarization challenge and local stablecoins opportunity

Africa’s heavy reliance on the U.S. dollar for trade and finance including through USD-denominated stablecoins leaves economies vulnerable to cycles of currency devaluation and high transaction costs. Large foreign reserves in USD also further weakens local currencies. While USD stablecoins improve transaction efficiency, they do not solve underlying dollarization risks. In fact, they risk concentrating control under U.S. financial institutions, reintroducing challenges such as sanctions exposure and systemic trust issues.

Although USD stablecoins are valuable for connecting African economies to global markets, full dollarization cripples economic growth and autonomy. A more sustainable path forward is to integrate African local currencies into on-chain financial systems, ensuring their continued relevance in a digital economy.

Nigeria has taken a significant step in this direction with the introduction of cNGN (Compliant Naira), the country’s first regulated stablecoin. Unlike the government-issued eNaira, cNGN is privately issued by Wrapped CBDC Ltd while following regulatory guidelines. This stablecoin maintains a 1:1 peg with the Nigerian Naira, providing a stable digital representation of the national currency. As of September 2025, more than 1.1 billion cNGN have been traded on local exchanges, unlocking new economic opportunities for users and businesses alike. As regulatory frameworks mature and institutional participation deepens, local stablecoins are likely to become more integrated with mainstream financial systems.

Conclusion

Each layer of the stablecoin value chain has an important role in the evolving system that is quietly reshaping access to financial services worldwide. While much of the profit still flows to institutions at the top of the chain in developed markets, the most profound impact is increasingly being felt across emerging economies.

Regulators, as enablers define the rules that issuers work with and how they can be integrated into local economies. Issuers like Tether capture the bulk of profits, earning billions of dollars in yield from reserves invested in U.S. Treasuries, while every new user holding USDT adds to that global float. Custodians and exchanges also monetize spreads and transaction fees along the way. At the end of the chain are retail users, especially in emerging markets who drive adoption using stablecoins for remittances, savings, and cross-border trade. Yet they absorb costs through on/off-ramp fees, volatility risks, and regulatory clampdowns. For example, a Nigerian freelancer may accept payment in USDT to bypass expensive banking rails, but still pays a 2–5% spread when converting back to naira, while Tether quietly earns on the reserves backing that same token.

In this sense, the stablecoin value chain delivers a new financial access to millions in emerging markets, but much of the upside remains concentrated with issuers and intermediaries in developed markets. On the other end, emerging markets are shaping how stablecoins get adopted, distributed, and trusted on the ground. However, for this potential to be fully realised, the value chain needs to become more inclusive and distributed, locally anchored, and built with more regulatory clarity in mind.

Disclaimer: This post is for informational purposes only and does not constitute legal, financial, or investment advice.