The Agentic Stack: AI Agents x Crypto Rails in Emerging Markets

AI agents plus crypto rails will reach the customers every existing payment system was built to leave behind, and they will reach them in emerging markets first.

Introduction

Over the past year, AI agents have moved from chatbot demos to autonomous systems that browse, decide, and transact on a user’s behalf. OpenAI and Anthropic are shipping production agents, Google has woven agents into Gemini and Search, and providers like Coinbase, Circle, and Cloudflare are building the rails these agents need to pay each other. The direction is consistent: a payments layer designed for software, not humans, built around stablecoins, programmability, and machine-speed settlement.

This article makes one argument. Existing payment rails were built for transactions large enough to carry a human’s cost: a salesperson, a credit officer, a card-network fee. Wherever the value of a transaction fell below that cost, the rail never got built and the customer went unserved. Agents collapse that cost to almost nothing, so the first markets to flip are not the ones Silicon Valley is building for. They are the markets full of transactions that were always too small to serve, the empty surfaces where no human-led service could ever close the unit economics. We call this the empty-surface thesis.

The scale is already measurable. A recent Keyrock analysis found the total AI agents settlement figure to be over $73 million across roughly 176 million blockchain transactions between May 2025 and April 2026. The dollar figure is small; the transaction count is the part worth dwelling on. Most agent payments run between one and ten cents, a distribution that only emerges when software is paying software, because no human would bother to authorize a one-cent payment. The rails that can profitably carry a one-cent transaction are the same rails that can finally serve customers every existing payment system was forced to leave behind.

Agent payment volume for x402 and MPP combined hit ~$48M across 180M transactions in five months, then flattened, the category’s first inflection but not its last.

The infrastructure serving this flow is not one thing but a stack. x402 is the execution layer, where stablecoins move agent-to-merchant inside an HTTP request; Google’s Agent Payments Protocol is the authorization layer above it. Most coverage frames these as competing standards. They are stacked, and they converge on a single denominator: stablecoins, with USDC accounting for the large majority of agent settlement volume in Keyrock’s dataset. That concentration is strong evidence that crypto rails are winning this layer, and also its biggest single risk.

What makes the foundation durable is that it keeps growing when crypto prices fall. The McKinsey and Artemis analysis found roughly $390 billion in genuine stablecoin payments in 2025, up sixfold in two years, with B2B at 58% and growing more than 700% year-on-year. The network is being expanded by businesses settling invoices, not speculators chasing yield, which is the precondition the empty-surface thesis depends on: an agent economy cannot be built on rails whose volume swings with token prices, but it can be built on rails grown by treasurers.

And the empty surfaces those rails reach first are not in San Francisco. A Lagos developer can pay for global APIs without a US company. A Manila freelancer can get paid from abroad without surrendering a chunk to remittance fees. A Jakarta startup can rent AI compute one call at a time. None of this is hypothetical. It is happening now, and it is happening there first for one reason: each of these flows was always too small for a human-led service to reach profitably, even at emerging-market wages, and too small for a Stripe to underwrite. The cost of serving them exceeded the value of the transaction, so for decades they went unserved. Agents erase that cost, and the markets that were left out first are the markets that flip first.

The four-layer agentic stack

Most coverage of agentic commerce talks about it as one thing, “AI agents with crypto wallets,” and that framing makes the space look smaller and flatter than it really is. In practice, the agentic stack consists of four distinct layers, each at a different stage of maturity, and each moving at its own speed. Understanding the shape of the stack is the easiest way to see where the real opportunities are, because the layers do not advance in lockstep, and the bottlenecks are almost never where the headlines are looking.

The first layer is payments, the rail that lets one agent send money to another or to a service. Protocols like Coinbase’s x402 and Google’s Agent Payments Protocol live here, and the engineering problem they set out to solve, letting software send a stablecoin inside a single HTTP request, is largely solved. The interesting question is no longer technical. Onchain data from Artemis shows x402 still processes only about $28,000 in daily volume at roughly $0.20 per transaction, with a significant share flagged as non-organic rather than commercial. The better read is not failure but un-arrived demand, and the reason it has not arrived points back to emerging markets. a16z’s Noah Levine puts it well: traditional processors cannot underwrite the merchant. A tool with no website, no entity, and no track record cannot get a Stripe account, and that describes the agent exactly. It also describes the Lagos developer, which is why this layer and the empty-surface thesis are the same story. The protocols themselves are converging into commodities. The fight that decides this layer is the workflow above the payment, the orchestration of what an agent may do, when, and with whose money, where teams like Halliday are defining the surface and no winner has emerged.

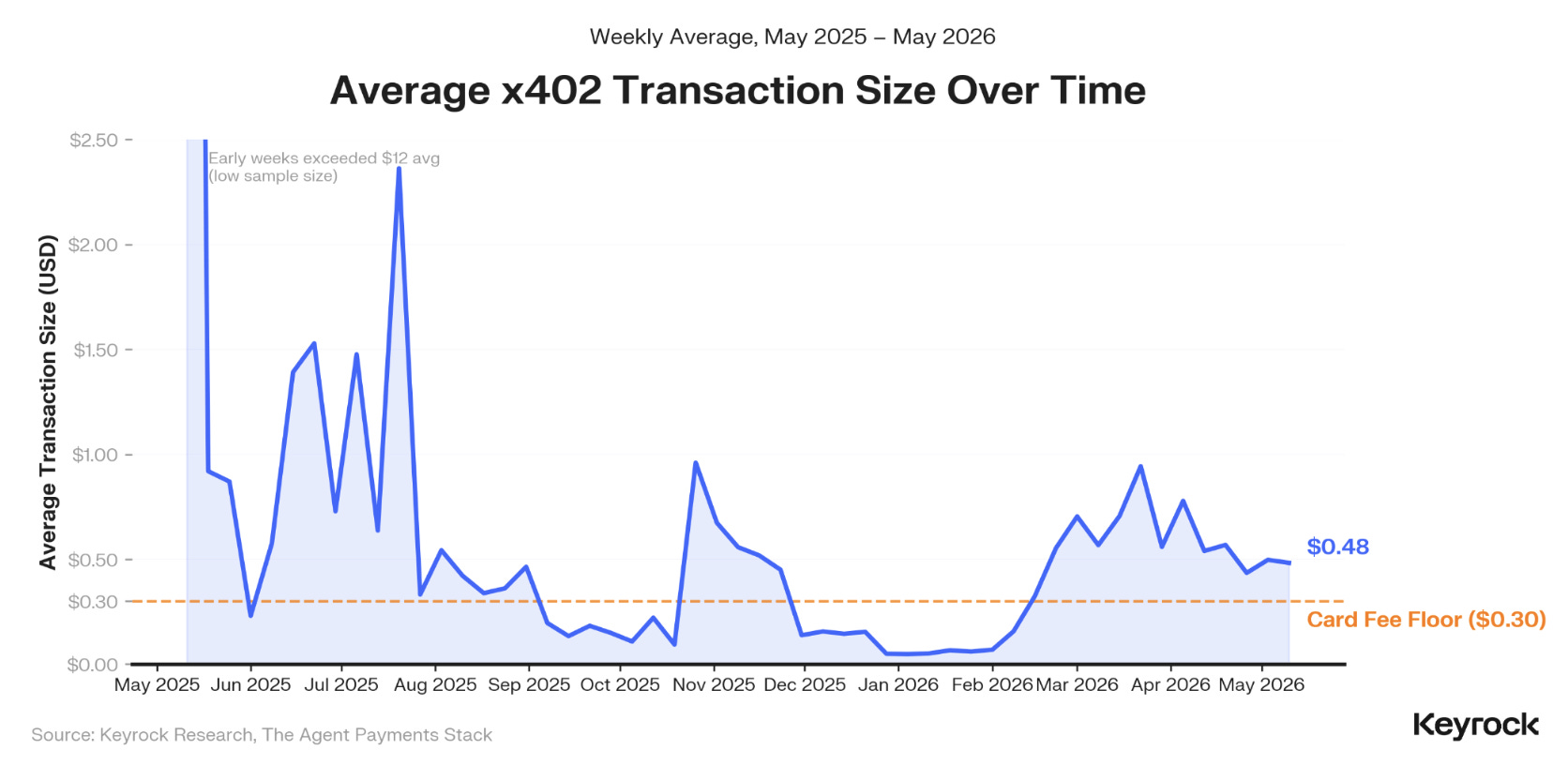

Average x402 transaction sizes have settled at $0.48, hovering right around the $0.30 card fee floor that traditional payment rails cannot profitably cross.

The second layer is identity and custody, where the agent gets a wallet and signs the transactions the payment layer carries. Coinbase’s AgentKit, Stripe (which acquired Privy in 2025), and Crossmint all ship production wallets. The interesting tension here is philosophical, not technical. There are two ways to give an agent the ability to spend money: let the agent hold its own keys for autonomous use cases like corporate treasury or recurring B2B flows, or keep the wallet with a human who grants the agent revocable scoped authority for consumer use cases like booking flights or managing subscriptions. The instinct in crypto circles is to call the first the “true” model and the second a compromise. We think that is wrong. Both are valid, they solve different problems, and the platforms that support both will likely absorb the long tail of agent use cases while the platforms that pick a side give up half the market by design.

The third layer is reputation, and we believe it is the bottleneck of the entire stack. The reason is structural. An agent’s track record today exists inside whatever platform issued it, an Uber-style rating on one marketplace, an API key history on another, and none of it travels when the agent leaves. The most credible design for portable agent reputation is onchain attestation, because anything else hands control back to a company that can gatekeep it. Primitives like the Ethereum Attestation Service and reputation systems like Ethos are live but were built for humans, not agents. The history here is worth taking seriously. Lightning Network micropayments, BAT’s browser monetization, and most decentralized compute marketplaces all promised new internet economies and struggled to attract sustained usage. The case that agent reputation is different rests on one specific claim: AI agents create non-human demand for portable trust that did not exist before, because no entity needed it. Whether that claim holds is the open question, and the first team to ship a default agent-reputation standard could own foundational infrastructure for the entire space. No clear standard has emerged yet.

The fourth layer is compute and data, which is really two layers crammed into one. Cheap inference is being commoditized fast by decentralized GPU networks like Akash and io.net, and an agent does not care whether its inference comes from AWS or Akash so long as it is cheap and available. The half that is genuinely contested is the data side. Most agents today operate on public information because they cannot safely touch anything private. A travel agent cannot read your bank balance, a medical agent cannot read your records, a trading agent cannot consume a proprietary signal feed without leaking it to the compute provider. Protocols like Nillion build verifiable private compute that aims to close this gap, and the reason it matters is practical rather than technical: without it, agents are a thin layer of automation over public APIs, and with it, agents can act on the parts of your life and your business that actually generate value.

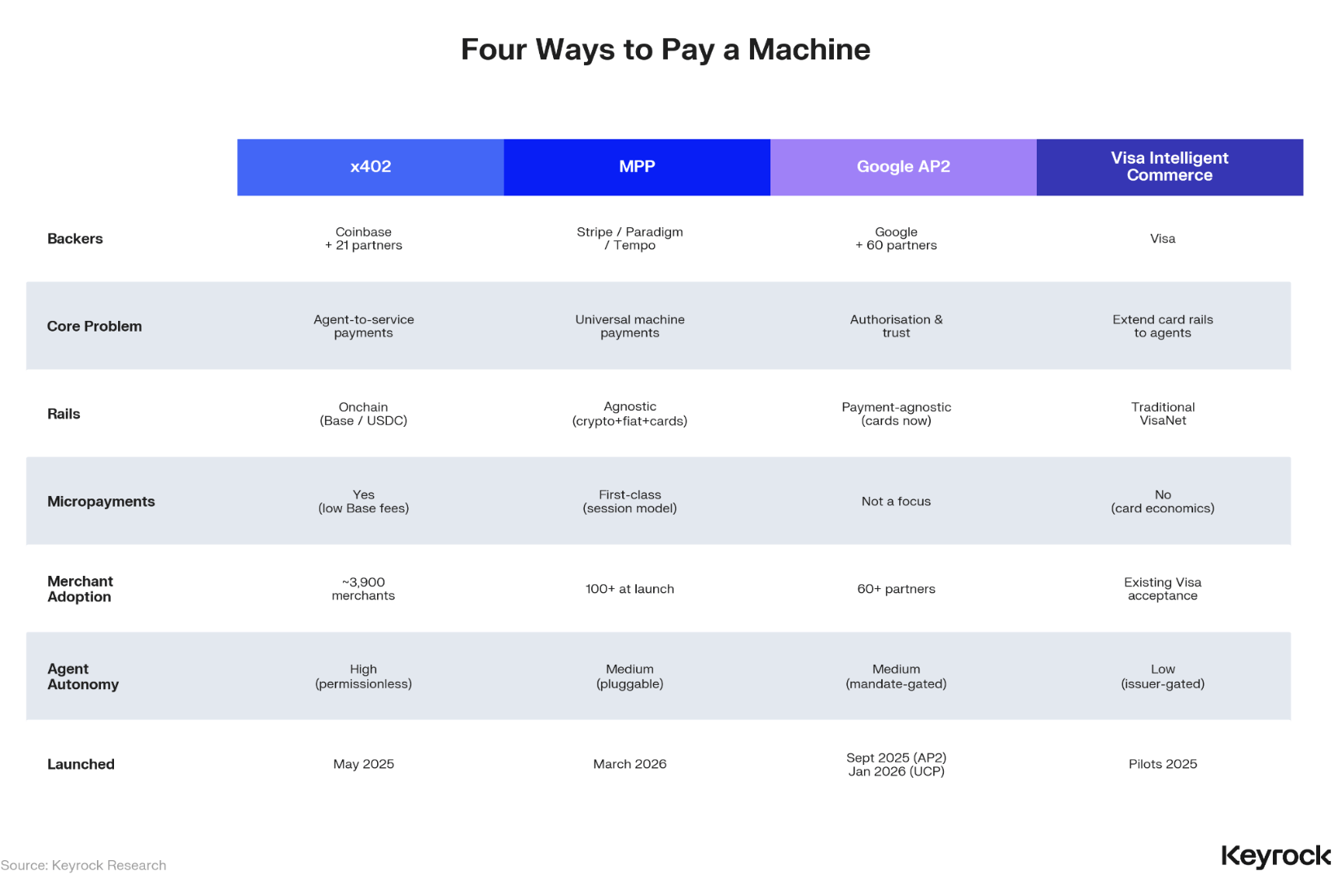

Four protocols, four different bets: x402 on permissionless micropayments, MPP on multi-rail flexibility, AP2 on authorization, Visa on extending card rails to agents.

The pattern across all four layers is consistent. The parts that look boring, workflow orchestration above payments, custody recovery, agent-reputation schemas, verifiable private compute, are the parts most likely to decide who wins. The flashier components, the protocols and tokens and partnership announcements that dominate the news cycle, are mostly commoditized already. Anyone covering agentic commerce by counting partnerships is measuring the wrong thing.

The agent economy is downstream of the stablecoin economy

Every layer of the stack covered so far quietly assumes one thing: that the unit of account is a stablecoin, not a fiat currency. An AI agent cannot hold INR, NGN, or BRL, because no bank will open a checking account for software with no legal entity, no KYC, and no human responsible for it. The agent holds USDC instead, and that single mechanical fact is what forces the entire stack onchain.

Three forces reinforce this. First, price stability, because an agent running a multi-step workflow cannot tolerate the asset it holds moving 5% mid-task. Second, global liquidity, because a Manila agent paying a São Paulo provider needs an asset that exists in both places with deep liquidity. Third, and most underweighted in public coverage, regulatory clarity. The GENIUS Act, signed in July 2025, gave US institutional capital a defined legal path into stablecoins. Stablecoin payment growth accelerated through the same period, and while the Act is not the only driver, the timing is consistent with regulated capital entering the market. MiCA had a parallel effect in Europe, pushing the market toward authorized stablecoins and supporting a non-USD stablecoin market that was marginal before.

Two findings from the a16z dataset complicate the easy story. Stablecoin velocity has roughly doubled since early 2024, from 2.6x to 6x, which a16z reads as the signature of a real payments network rather than a savings vehicle. And counterintuitively, the cross-border share of stablecoin payments is falling, not rising. Intra-country transactions grew from roughly 50% to 75% of payment volume in two years. Stablecoins are becoming local payments rails that happen to run on global infrastructure, and the agent economy is being built on top of that shift.

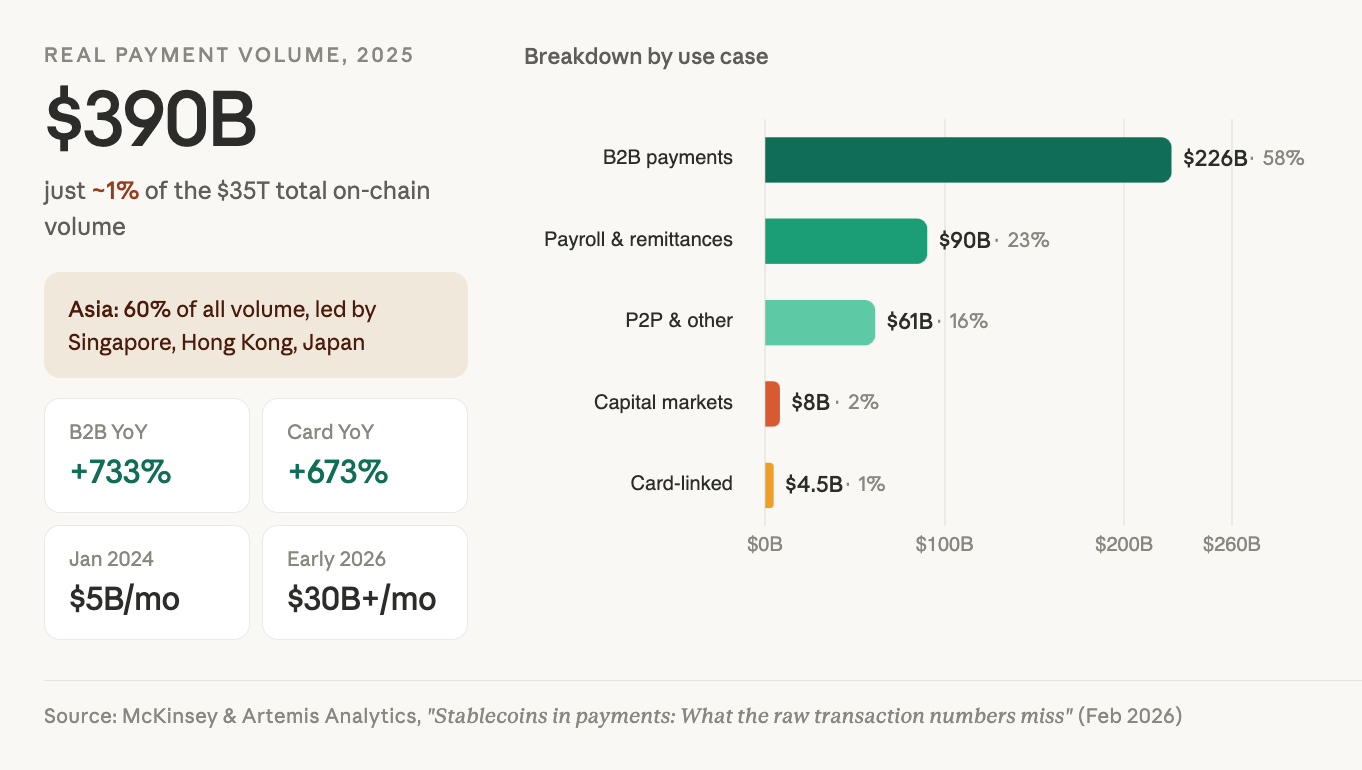

A 2025 chart showing stablecoin payment volume at $390B, dominated by B2B payments and concentrated mainly in Asia.

The thesis to take forward is that the agent economy is downstream of the stablecoin economy. Anyone predicting the geography of agentic commerce by looking at where the AI labs sit is looking in the wrong place. Look at where the stablecoins are already flowing.

Why agents will be EM-native, not Western-exported

The default story about the agent economy is that it will be built in San Francisco, scaled in San Francisco, and exported to emerging markets as a downstream consequence of Western AI dominance. We think this story is almost exactly backwards. Agents will be EM-native because the unit economics that make agents viable as a replacement for humans only work in markets where human-led services are too expensive to scale across the relevant surface. In the West, agents have to compete against humans and software already there. In EMs, the human service does not exist at the relevant scale because the unit economics never worked, which means the agent is not replacing a human but filling a gap that humans never could.

The obvious objection is that EM labor is cheap and abundant. The answer is that cheap labor is not the same as scalable labor. A credit officer handling 200 applications a month at ₹20,000 still costs roughly $1.20 in labor per application, which destroys the unit economics on a $180 loan with regulated interest caps. An agent making the same call costs a fraction of a cent. EM labor has been trying to close these gaps for years without success, because the underlying transactions are too small to support any human-delivered service. The agent does not replace the human. It fills the surface human labor was always priced out of.

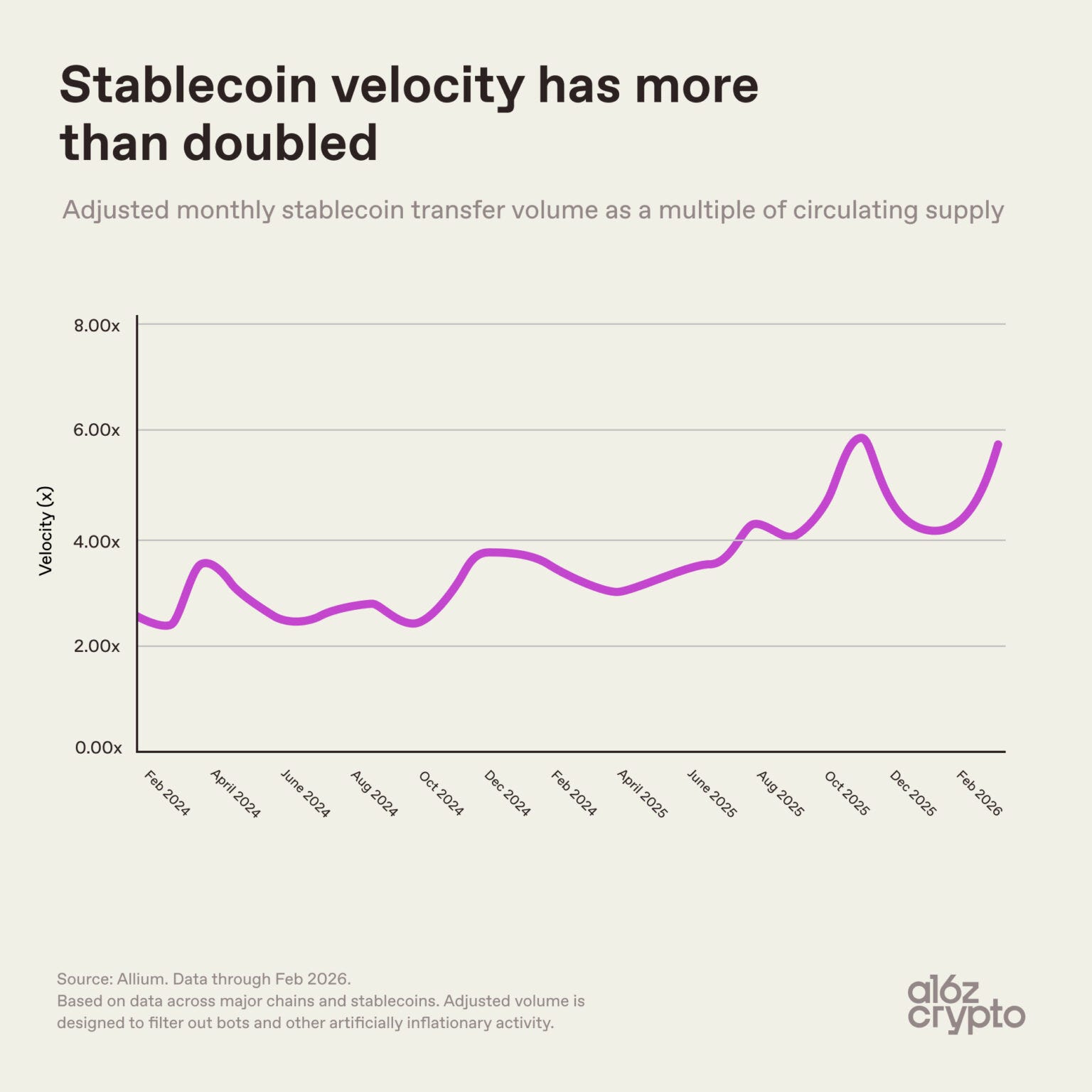

Stablecoin velocity more than doubling from early 2024 to early 2026, reaching roughly 6x circulating supply.

Stablecoin velocity more than doubling from early 2024 to early 2026, reaching roughly 6x circulating supply.

Sub-case one: vernacular voice agents underwriting micro-credit. India has 22 official languages and more than 1,600 dialects. No NBFC can hire enough vernacular credit officers to underwrite the long tail of micro-credit demand at sub-20% APR margins. Voice AI platforms such as Caller Digital, Bolna, and Gnani describe shipping voice agents for NBFC collections, KYC, and loan servicing across a dozen Indian languages, built to operate within RBI Fair Practices Code requirements. Paired with stablecoin-rail credit platforms like Jia, the combination points toward a stack that can close loans at economics no human-led NBFC could reach.

Sub-case two: agent-led remittance optimization. A worker sending money home today navigates four to seven possible corridors, from traditional remittance services at 6 to 8% all-in to stablecoin remittances that can settle in minutes at 1.5 to 2.5%. The fees and settlement times vary by hour, by liquidity depth, by P2P spreads, and by FX rate. A human cannot watch this market all day. An agent can, routing each remittance through the cheapest available path and capturing several hundred basis points that currently leak to whichever corridor the sender happened to default to.

Sub-case three: agent-mediated API access for EM developers and SMEs. A developer in Lagos or Jakarta trying to build a fintech today needs to consume a dozen foreign APIs (KYC, fraud screening, email, AI inference, mapping, document signing). Many of these are difficult to pay for without a US or UK business entity. The standard workaround is to incorporate in Delaware via Stripe Atlas, which carries an upfront cost plus several thousand dollars over the following years in registered-agent, franchise-tax, and filing fees. With a stablecoin wallet, a developer’s backend can pay foreign APIs per-call through x402, with no account, no card, and no entity required.

Sub-case four: intent-orchestrated B2B transactions across Africa’s fragmented payment rails. Africa’s B2B payments market is estimated to exceed $200 billion annually, with SMEs making up the large majority of businesses across the continent. The structural problem is that a meaningful share of recurring transactions fail across African markets because no one is watching which provider is underperforming in real time. An agent can. NjiaPay, which raised $2.1 million in March 2026 to expand its payment-orchestration layer across the continent, describes routing each transaction to the best-performing provider in real time and is building toward agents that let merchants query their payment data conversationally. The human-staffed equivalent does not exist at this surface. The agent is not replacing it. It is the first version of it.

The pattern across all four is the same. The agent is not a better version of an existing service. It is the first version of any service at all for these surfaces. The West will likely be the laggard, not the leader, on mass-market agent deployment, because Western surfaces are already too well-served by existing humans and software for agent unit economics to compete.

India proves the thesis and breaks it at the same time

India is the most interesting test case for the agentic stack, and the one place in this article where the broader argument bends. The earlier claim was that crypto rails are the only stack that closes the agent payment loop end-to-end. India is the case where a sovereign rail does the same job inside one country, because the government built a real-time programmable payment system before crypto could fill the gap. The clearest proof point arrived on February 20, 2026, at the India AI Impact Summit, where Razorpay and NPCI announced a pilot bringing agentic payments to Anthropic’s Claude, letting a limited set of users order from Zomato, Swiggy, and Zepto inside the conversation itself. The pilot is built on UPI Reserve Pay. This was not Razorpay’s first such step: at Global Fintech Fest 2025, Razorpay and NPCI ran a comparable agentic-payments initiative with OpenAI, so the Claude pilot is best understood as a second integration on the same underlying rail rather than a one-off. Separately, vernacular voice-AI providers like Gnani are building agents that complete UPI payments inside live customer calls in Indian languages.

The contradiction this creates is unresolved. The RBI position is “blockchain yes, crypto no,” and Governor Sanjay Malhotra has been explicit that India does not need to respond to US stablecoin innovation because UPI already does the job. He is right for domestic flows. He is wrong for cross-border agent commerce. Consider, illustratively, an Indian developer’s agent that needs to pay a US inference provider per call: UPI cannot settle that flow. The Indian agentic stack is bifurcating in real time: UPI for domestic, stablecoins for cross-border. The COINS Act 2025, the model law drafted by Hashed Emergent in collaboration with Black Dot Public Policy Advisors proposes a Crypto Assets Regulatory Authority, is the first serious effort to contemplate a regulatory framework for the cross-border half of this stack, though the substantive regime still depends on enactment and implementing regulations.

Compliance is the hardest unsolved layer, and only the easier half is being built

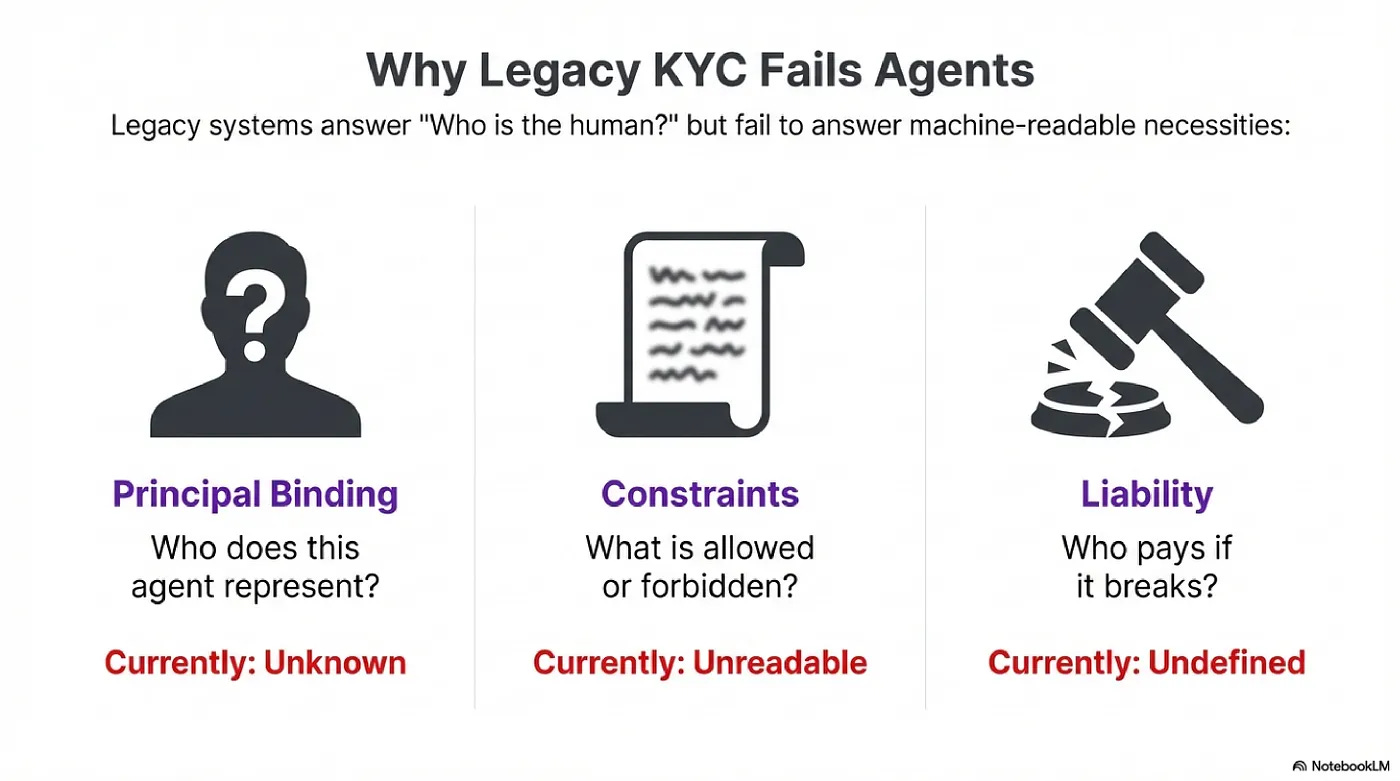

If India shows how sovereign rails handle the domestic half of agent commerce, the compliance question is where the cross-border half runs into a wall. Every existing AML and KYC framework was built around a single assumption: every account has a natural or legal person behind it, and a regulator can chase that person if something goes wrong.

Agents break this assumption in two ways. At account opening, agents have no legal personhood and no biometrics, which means either the developer wraps the agent in their own KYC and inherits the liability, or the system invents new agent-specific identity primitives. At transaction monitoring, AML rules trigger on patterns derived from human behavior (round numbers, structuring below reporting thresholds, unusual times of day), and agent activity looks nothing like that, which means existing systems either flood compliance teams with false positives or miss real risk because legitimate agent flows are anomalous by definition.

McKinsey’s 2026 State of AI Trust survey found fewer than one in three organizations have adequate governance to oversee AI agents that are already initiating payments and executing compliance decisions in production. The agents are deployed. The compliance layer is not. The clearest early mover is Singapore, which launched the Model AI Governance Framework for Agentic AI at the World Economic Forum in January 2026 and followed it in April with MetaComp’s open Know-Your-Agent (KYA) framework, which extends FATF Travel Rule principles to agent-to-agent transactions through four pillars: agent identity, permission control, behaviour monitoring, and ecosystem governance.

KYA is the right starting point, but it is only the first half of the problem. It solves credentialing, which is technically tractable. The harder half, AML monitoring for autonomous machine-to-machine transactions at sub-dollar amounts below every existing reporting threshold, has barely been started anywhere. Other jurisdictions are moving in adjacent directions, UAE through ADGM, India through UPI’s existing compliance rails, Kenya and Brazil through crypto VASP regimes, while the US and EU look slower to adapt because the GENIUS Act covers stablecoins but not agents, and the EU AI Act largely defers agent-liability questions. The compliance collision is not coming. It has arrived, and KYA is the first answer to it, but only the first half.

What we believe is investable

The four-layer framework is a map of where capital is concentrated, where it is missing, and where the returns will compound. Each layer is at a different stage of maturity and rewards a different kind of capital, and the single most expensive mistake we see investors make in this cycle is treating the stack as one bucket called “agent infrastructure.” The instinct is to back the horizontal protocol everyone will use. The sharper bet, almost everywhere in the stack, is the opposite. Protocols commoditize. The margin accrues to whoever owns the borrower, the merchant, the regulatory license, and the local language, and rents the agentic stack underneath. The defensibility was never the technology, which any competitor can buy. It is the domain knowledge to underwrite a surface everyone else priced as too small. The winners will look less like crypto companies and more like operators who happen to run on rails. That principle plays out differently in each of the four layers.

Payments is the most mature layer and the most institutionally backed. Coinbase, Stripe, Google, Visa, and Cloudflare are all building credible rails, and the protocols are settling into commodity status, which signals the category has crossed from speculative to real. The opportunity for new entrants is no longer in the protocol layer but in workflow orchestration above it, where teams like Halliday are still defining the surface.

Identity, custody, and reputation is the layer most investors are reading too narrowly. At the enterprise security level it is well-capitalized through companies like Didit and Defakto, and rightly so. The version we are most active in is the adjacent one: the compliance and assurance infrastructure that connects agent identity to regulatory reality. As agents move into regulated workflows, demand for verifiable, audit-ready infrastructure outpaces what human compliance teams can deliver.

Compute and data has matured into a category with clear leaders. Akash and io.net have crossed escape velocity, and the most interesting frontier now sits inside verifiable private compute, where Nillion is defining a sub-layer the rest of the stack will eventually depend on.

The fourth layer is the most under-priced: verticalized agent applications in emerging markets. This is where the principle above lands hardest. There is no incumbent to displace, no Western analog to copy, and no horizontal protocol that can substitute for owning a specific borrower in a specific language under a specific regulator. The defensibility is the domain knowledge to underwrite a surface everyone else priced as too small.

What we are already backing

Four of our portfolio companies are already building inside the layers above, each proving a different piece of the broader thesis.

Jia is positioned at the intersection of the fourth opportunity and the stablecoin denominator. It is building toward AI-underwritten stablecoin credit in emerging markets, originating loans in segments where human-led NBFCs have never closed unit economics. Like any early-stage credit business in a new asset class, its portfolio metrics will be tested across multiple cycles. The structural argument holds either way: micro-credit has been the textbook case of a market where human underwriting could not reach the long tail, and Jia is early evidence that AI-led underwriting on stablecoin rails can.

Spydra anchors the identity and compliance layer, having expanded from RWA tokenization into AI-based assurance and compliance tooling. As agents enter regulated workflows, audit-ready assurance is exactly where demand lands first.

Jina operates alongside Spydra in the compliance layer, building AI-powered browser agents that automate KYB onboarding, investigations, and ongoing monitoring for stablecoin and fintech companies. The compliance collision the article describes is happening in production today, and the work is being absorbed by human analysts running the same investigation playbook over and over. Jina is turning those playbooks into agent-executed workflows, which is what makes regulated agent commerce operable at machine scale.

Reclaim Protocol sits in the identity and verification layer, building infrastructure that lets users carry verified credentials (education, employment, finance) across services without surrendering control to the platform that issued them. AI runs much of the verification workflow with zero-knowledge proofs in the backend, which is the hybrid pattern the article’s third prediction describes: rules off-chain, receipts on-chain. The agent reputation primitive the stack needs has not been built yet, but the human-side primitive Reclaim is building one of the closest live analogues.

Three predictions

Agent payments will cross from experiment to infrastructure by end-2027. The headline numbers today overstate the category, by Keyrock’s and a16z’s reading, a large share of late-2025 x402 dollar volume was non-organic rather than real commerce. Strip that out and genuine agent settlement is a few million dollars a month. By December 31, 2027, organic agent payments will cross $500M annualized, a roughly 50x jump from the cleaned baseline. The reason is structural: traditional rails cannot profitably process a 10-cent transaction but most agent payments are exactly that size, and as real services get priced per-call on stablecoin rails, the productive volume outgrows the gamed volume.

The first regulator-approved agent-originated loan in an emerging market will be issued in the Philippines before end-2027. By “agent-originated” we mean a loan where an AI agent handles the lending decision through to disbursement (underwriting, approval, and issuance) under a licensed entity, not merely agent-assisted servicing or collections. This may not be seen in Kenya, where digital lending defaults are too high to support unsecured agent underwriting. Not Brazil, where the central bank significantly restricted stablecoin use for cross-border settlement through regulated channels via Resolution 561 in April 2026.The Philippines is the rare market where three things line up: a working local-currency stablecoin (PHPC) that has graduated from the central bank sandbox, licensed digital banks with sharply improved bad-loan ratios over the past 18 months, and a regulator that has invited AI and crypto into sandbox cohorts.

Agent identity will run on two layers, not one, by mid-2027. Every agent needs a way to prove who it is and what it is allowed to do, and two answers are emerging in parallel. Off-chain, regulators are writing rule-books like Singapore’s governance framework that define what agents can do inside regulated systems. On-chain, standards like ERC-8004, live since January 2026 with thousands of agents already registered, give each agent a public record of its activity. Most coverage assumes one model will win. It will not. Regulators will define the rules off-chain, the chain will provide the receipts, and Mastercard and Visa are already running both in parallel.

What can break this

No thesis in this space survives without naming what could undo it. Three risks deserve direct treatment, because each one could materially change where this lands.

The first is regulatory crackdown. The EU AI Act’s high-risk provisions become enforceable on August 2, 2026, and the prevailing legal reading is that autonomous agents executing financial transactions are likely to fall inside the high-risk category by what they do, not by their model architecture, though that classification has not been settled by enforcement yet. This means the category is one bad incident away from a defensive regulatory response that gets locked in for years. The RBI is a credible second source given its stance on private stablecoins. If either jurisdiction freezes cross-border agent flows for compliance reasons, the EM agent economy bifurcates further: domestic flow continues on local rails, but the cross-border thesis that animates the rest of this article stalls until the framework catches up.

The second is an agent failure cascade. The category has already had its first warning shot, when an attacker drained roughly $170K from an AI-linked wallet on Base in May 2026 by sending Grok a Morse code prompt that tricked it into authorizing a token transfer. The incidents have been small enough to absorb so far, but the failure mode is structural: agents are non-deterministic systems with access to deterministic financial rails, which means the next incident is a question of scale, not probability. A nine-figure loss involving a major LLM and a real user base would shift the conversation from “how do we accelerate agent commerce” to “how do we restrict it,” and the political pressure that follows is harder to reverse than the technical fix.

The third is foundation model collapse into closed ecosystems. If OpenAI, Google, or Anthropic ship vertically integrated agent stacks good enough and cheap enough that the average developer never leaves them, the open coordination layer this article argues for becomes a niche rather than a default. Several labs are already moving in that direction. The honest version of the counterargument is not that the open layer always wins, it is that the open layer wins specifically for cross-platform commerce, where no single lab can credibly be the neutral broker. If cross-platform commerce turns out to be a smaller share of agent activity than expected, the open thesis is significantly weaker than this article has assumed.

Where the next decade lands

The agentic stack is the machine economy in its most concrete form: software acting on its own behalf, in real markets, with real money, on rails that did not exist five years ago. Hashed Emergent’s thesis on the onchain and machine economy frontier across India and emerging markets is built on the observation that this stack will not arrive uniformly. The structural conditions for early agent deployment, large underserved surfaces, weak legacy alternatives, and unit economics that finally close at machine cost, are most concentrated in markets like India, Brazil, the Philippines, and across Africa. That does not mean the West will not lead in enterprise and developer-tool categories, where it almost certainly will. It means the consumer-scale agent economy has more room to grow where the existing economy left the most space behind.

The protocols will keep evolving. The regulations will keep moving. The data will keep getting cleaner. But the structural argument does not change: agents land first where the gap they fill is largest, and that gap is where the next decade of builders, founders, and capital will increasingly focus.

The first billion agents will not look like the last billion users.

well structured and well written!

I recommend this to my coworkers!