Stablecoins: Leapfrogging Africa’s Financial System

Stablecoins are transforming finance in Africa, offering a powerful upgrade to traditional systems. This article explores how they drive the next wave of financial innovation across the continent.

Our world has shifted from isolated local economies to a deeply interconnected global system, yet the financial rails that support it in Africa haven’t evolved at the same pace. Traditional financial systems have failed to deliver stability, accessibility, and efficiency, leaving people exposed to inflation and financial uncertainty, with limited control over their savings or access to global markets. But just as the region leapfrogged desktop computers and moved straight to mobile, it’s now positioned to leap past outdated banking infrastructure and embrace stablecoins instead.

Africa is the fastest-growing region for crypto adoption, according to Chainalysis, with a year-over-year (YoY) growth rate of 45% from 2022–2023 to 2023–2024, surpassing other emerging markets like Latin America at 42.5%. This rapid growth highlights the huge potential for stablecoin adoption, especially in a region where banking penetration remains among the lowest globally.

With mobile money already deeply embedded across Africa, stablecoins offer a natural evolution by providing a seamless way to access financial services using just a mobile phone. Africa has the highest mobile money adoption in the world, proving the demand for alternative financial solutions. Stablecoins can build on this foundation, expanding financial inclusion and enabling more efficient, borderless transactions.

In the last three years, stablecoins have become an integral part of Africa’s financial system, providing a reliable way to store value, send money across borders and conduct trade without relying on volatile local currencies. Dollar-backed stablecoins like USDT and USDC are filling the gaps left by traditional finance, giving people access to a stable store of value in economies where U.S. dollars are scarce. Looking ahead, we believe that in 10 years, more people in Africa will have crypto wallets and use stablecoins for daily transactions than traditional bank accounts.

This article explores how stablecoins are transforming Africa’s financial landscape, breaking down the challenges of traditional finance, highlighting real-world use cases and showcasing the key players building this ecosystem. Through a country-level analysis of Nigeria, South Africa and Kenya, we explore the regional drivers of adoption and regulatory developments. Whether it’s businesses making global transactions, individuals protecting their savings from inflation, or entire industries moving to stablecoin rails—one thing is clear: this is just the beginning of stablecoin adoption.

Stablecoins are transforming cross-border payments in Africa

As Patrick Collison, CEO of Stripe, has noted, stablecoins are “room-temperature superconductors for financial services.” They will allow businesses to pursue new opportunities that could not otherwise survive the burden of incumbent payment rails or the friction of traditional gatekeepers.

Nowhere is this more clear than in cross-border payments, where traditional systems are slow, expensive and reliant on multiple middlemen. High fees and long delays make transactions complicated—especially in Africa, where the average remittance rate is around 8% and financial infrastructure is often limited or absent. Before we get into how stablecoins are changing cross-border payments in the region, we need to first look at the existing financial rails and the challenges they create.

Traditionally, cross-border payments work in two main ways:

Netting-Based Payments (For Consumers): Platforms like TransferWise and Remitly use a system called netting. Instead of moving money across borders, they keep funds in different countries and adjust balances internally. For example, if someone in India sends money to Nigeria, the platform deducts the amount from its Indian balance and adds it to its Nigerian balance. No actual money moves between countries—it’s just smart treasury management that reduces delays. This method allows for fast transfers but requires companies to hold large amounts of money in multiple countries. The cost usually falls between 75 to 100 basis points.

SWIFT-Based Payments (For Businesses & Institutions): Large international payments go through SWIFT, a messaging system banks use to communicate transaction details. But SWIFT itself doesn’t move money—it just sends instructions, and the actual transfer happens through a chain of correspondent banks. If someone in the US sends money to Nigeria, the payment typically travels through multiple middlemen—starting with a local bank, then moving through foreign exchange dealers and intermediary banks before reaching the recipient’s account. Each of these steps adds delays, increases costs, and creates points where transactions can get stuck. A simple transfer can take two days or more, and by the time it reaches the recipient, fees can add up to 150 to 300 basis points.

These traditional payment systems don’t work very well in Africa for several reasons. Netting-based models depend on companies holding large capital reserves in multiple countries, which is difficult due to strict foreign exchange controls, liquidity shortages, and volatile local currencies. This makes it expensive and impractical for payment providers, while also being capital-inefficient, limiting their ability to scale effectively across markets.

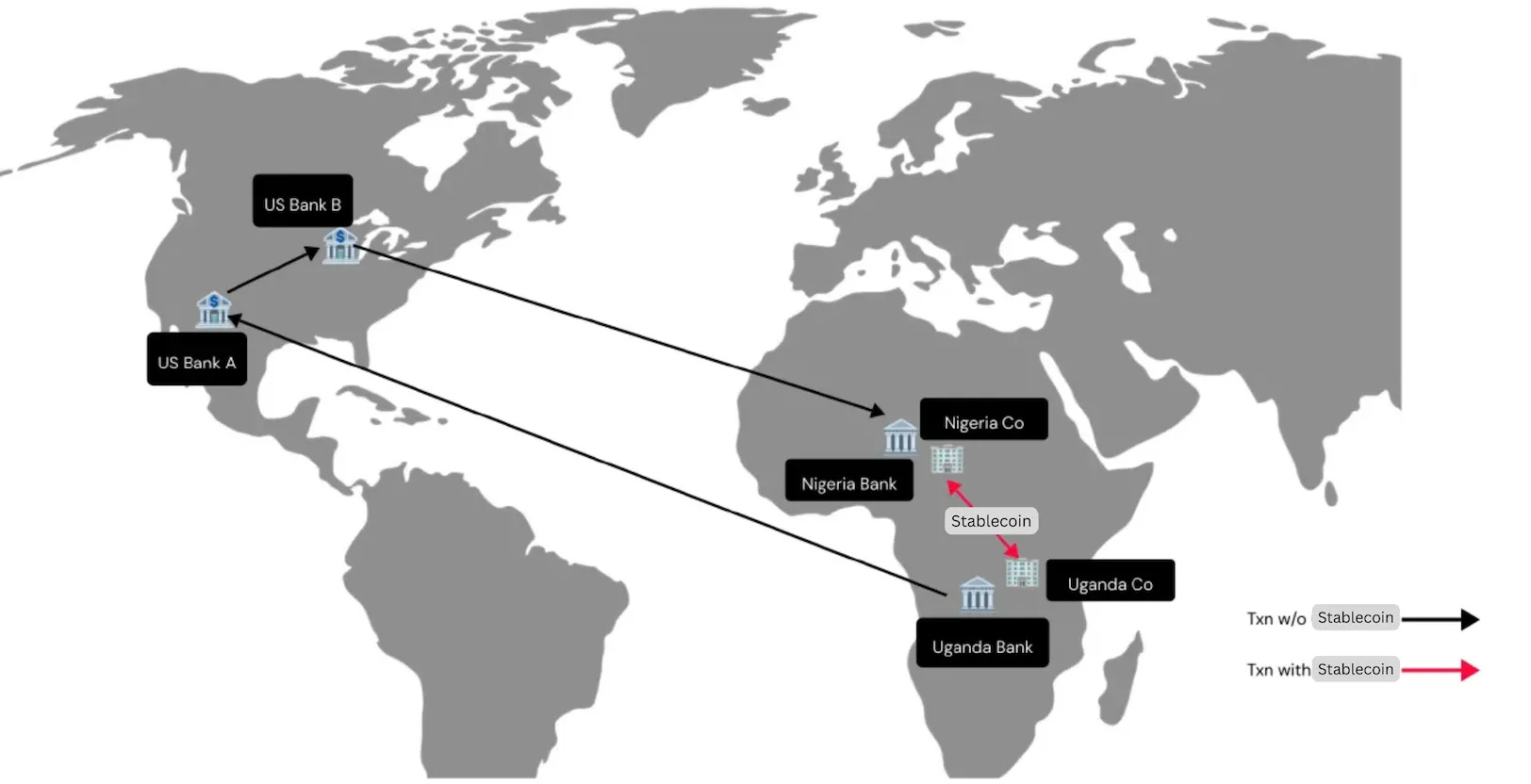

SWIFT-based payments face even bigger challenges. Many African banks lack direct connections to global banking networks, forcing transactions to pass through multiple intermediaries in Europe or the U.S. before reaching their final destination, as shown in the image below. Each step adds fees, delays, and the risk of funds getting stuck due to compliance checks or unexpected regulatory roadblocks. On top of this, a significant portion of the population is unbanked, meaning many people don't have access to basic financial services like savings accounts, credit, or insurance at all.

Stablecoins offer a way around these problems by enabling real-time, low-cost transfers without needing large capital reserves or bank intermediaries. Instead of routing payments through multiple intermediaries, a user in the U.S. can convert dollars into stablecoins and send them directly to a user in Nigeria, who then converts them into NGN and accesses the funds locally.

This process eliminates the inefficiencies of SWIFT and netting-based models, as transfers occur directly through exchanges or blockchain wallets connected to on-ramp and off-ramp providers. These providers integrate with local payment systems, such as ACH in the U.S. or Opay in Nigeria, enabling seamless conversions between stablecoins and local currencies.

Unlike traditional methods, which are slow and expensive, stablecoin transactions settle in real time, with fees as low as 10 to 50 basis points—making them not only cheaper but also more reliable and accessible across Africa’s fragmented financial landscape.

While this method works well for consumers and remittances, businesses benefit more from using stablecoin infrastructure providers. These providers handle the complex requirements—maintaining local accounts, ensuring regulatory compliance and managing KYC/AML requirements for both senders and recipients.

Recently, Stripe acquired Bridge (a stablecoin API provider) for $1.1 billion—just two years after its launch in 2022—to strengthen its global stablecoin payment network. Africa is a major market for Bridge, enabling stablecoin payouts for most African payment companies operating across Europe, the U.S., and Asia. This highlights the growing demand for stablecoin infrastructure and how quickly key players in the space are scaling.

While Bridge has laid the groundwork for stablecoin orchestration and issuance, there’s still significant work to be done in this sub-sector. Cross-border payments remain a massive opportunity, and several key problems need solving. Here are several high-impact areas where builders can focus, though this list isn't exhaustive:

Remittances: Sending money home is one of the most common cross-border payment needs, yet traditional rails make it costly. In 2023, global remittance flows hit $883 billion, with fees that disproportionately impact low-income users. Today, sending $200 from the U.S. to Nigeria costs less than $0.01 via stablecoins, compared to $7.60 using traditional methods. Reducing these costs at scale remains an urgent need.

Payouts: Cross-border micropayments remain expensive and inefficient for freelancers in the gig economy. In places like Kenya, some individuals even resort to "renting" PayPal accounts because setting one up themselves is too difficult—highlighting how access barriers compound the already high costs of sending or receiving small international payments. Stablecoin rails could significantly benefit these workers by simplifying payments. In addition, businesses operating across multiple countries can use stablecoins to efficiently manage cash flow and seamlessly pay employees, clients, or suppliers worldwide.

Repatriation: Some of the largest global companies selling goods and services in Africa can use stablecoins to move money back to their home country. With stablecoin infrastructure, funds can settle in under 30 minutes instead of the 2-3 days required by traditional payment rails.

Intra-continental Trade Payments in Africa: Intra-African trade accounts for only 15% of the continent's total imports and exports—far below North America's 54%, Asia's 60% and the European Union's 70%. A major reason for this imbalance is the lack of direct currency conversion infrastructure—most trades require converting local currencies to dollars, pounds, or euros before swapping into another African currency. This inefficiency adds $5 billion a year in unnecessary costs to intra-African transactions. Solving this is crucial to unlocking frictionless trade across the continent.

Global Aid: Today, only around 40 cents of every dollar donated to a global aid organization reaches the final recipient, with the rest lost to multiple intermediaries. There’s a clear need for a more efficient, low-cost system to deliver global aid transparently and seamlessly.

All these use cases need better solutions and point to a future where stablecoins become the default for cross-border payments—whether for consumers or businesses. The question is no longer if this shift will happen, but how it will take shape. The speed and effectiveness of this transition will depend on how well companies build the necessary infrastructure, navigate regulations and refine the user experience. Those who solve these challenges first will define the next generation of global cross-border payments.

Stablecoins are protecting savings from inflation and currency devaluation in Africa

Stablecoins are gaining traction in regions where dollar banking is inaccessible, inflation is high and fiat payment networks are either too expensive or unreliable. Africa reflects these conditions, making stablecoins a critical tool for protecting savings and maintaining purchasing power in economies where local currencies continue to lose value.

Currency devaluation is one of the biggest financial challenges in African markets. Take the Kenyan shilling, for example—it has lost 50% of its value against the U.S. dollar, despite Kenya’s GDP tripling between 2008 and 2024. The contradiction is clear: economic growth is rising, but confidence in the local currency is not. Similarly, in Nigeria, inflation and naira depreciation have been key drivers of stablecoin adoption. The naira hit a record low in February 2024 and has been struggling ever since, reinforcing the need for a stable alternative.

As local currencies continue to lose value, stablecoins are emerging as the preferred hedge, offering a more reliable way to transact and store wealth. Unlike cash or gold, stablecoins provide a fully digital, widely accessible payment rails that doesn’t rely on banks, payment networks, or central banks. Additionally, users in emerging markets who hold dollar-backed stablecoins gain indirect access to U.S. financial instruments, such as short-term Treasuries—something previously out of reach for most. Over time, governments may also launch their own local stablecoins, which could help build trust and drive the adoption of local currencies.

Local stablecoins have the potential to stabilize economies, expand financial access, and reduce reliance on the dollar in emerging markets by offering a trusted alternative to both cash and volatile crypto. The Central Bank of Nigeria recently approved cNGN, the country’s first regulated stablecoin, granting it a provisional license in 2024. This signals a growing shift toward local currency-backed stablecoins, which will soon integrate into the web3 ecosystem, driving adoption, better price discovery, and more efficient on-chain transactions.

Currently, dollar-based stablecoins are the preferred choice for users in emerging markets. They serve not only as a hedge against currency volatility but also offer higher yields than traditional savings accounts—making them an attractive option for Africans looking to preserve and grow their wealth. While conventional banks offer low interest rates, stablecoin savings platforms leverage decentralized finance (DeFi) and crypto lending models to generate much higher returns for users.

For example, Busha Earn, a Nigerian crypto platform, allows users to save their stablecoins with yields of up to 7.5% annually, significantly higher than what most Nigerian banks offer. This makes stablecoin savings an attractive option—not just because of the higher interest rates, but also because users are earning on top of the value preserved by hedging against currency depreciation. This combination makes stablecoins a powerful tool for both wealth preservation and growth.

Sub-Saharan Africa leads the world in DeFi adoption, likely driven by the growing need for accessible financial services in a region where only 49% of adults had a bank account as of 2021, according to the World Bank. This shows that stablecoins aren’t just an alternative—they’re becoming essential for financial stability in regions where traditional systems are failing.

Stablecoins are unlocking affordable credit for MSMEs in Africa

Africa has a $330 billion credit gap, leaving millions of individuals and small businesses without access to formal financing. This lack of affordable credit limits their ability to sustain daily operations and contribute to economic growth.

In these markets, small businesses are often overlooked by traditional financial institutions due to high collateral requirements, lengthy documentation processes and a lack of credit history. With limited access to affordable upfront capital, many micro, small, and medium enterprises (MSMEs) turn to informal lenders for financing.

In the web3 space, stablecoin-based lending protocols have demonstrated significant potential over the past three years in addressing this issue. However, most of these solutions remain overcollateralized, requiring ~150% collateralized crypto assets, which effectively excludes MSMEs in emerging markets. While undercollateralized lending protocols like Goldfinch have emerged, they primarily serve as alternative debt providers for fintech lenders rather than directly catering to small businesses on the ground.

Recently, two companies—Jia and Haraka—have been actively working to disrupt this space and capture the market opportunity in Africa. These companies provide blockchain-based loans to small businesses, rewarding responsible borrowers with ownership, thereby enabling them to build wealth and drive economic progress within their communities.

Bringing this real-world economic activity on-chain benefits both the investor and the borrower. Investors get democratized access to real yield, while borrowers get access to blockchain liquidity, with ownership as a mode to long-term wealth creation for themselves and their communities. The use of blockchain also reduces the large transaction costs (typically passed on to the end borrower) often associated with private credit markets, and enables the creation of on-chain credit histories for borrowers to build reputation over time.

Nigeria is at the epicenter of crypto activity in Sub-Saharan Africa

Africa’s most populous nation is leading the charge in stablecoin adoption, driven by a dynamic fintech sector and significant economic challenges. Nigeria’s economy has faced a series of shocks in recent years. Depressed oil prices—a key driver of its export economy, combined with the impact of COVID-19 and supply chain disruptions have led to prolonged financial uncertainty. The country suffers from one of the highest inflation rates in Africa, worse than the entire Francophone region. As the Naira continues to weaken, stablecoins have become a vital tool for Nigerians looking to preserve wealth and transact globally.

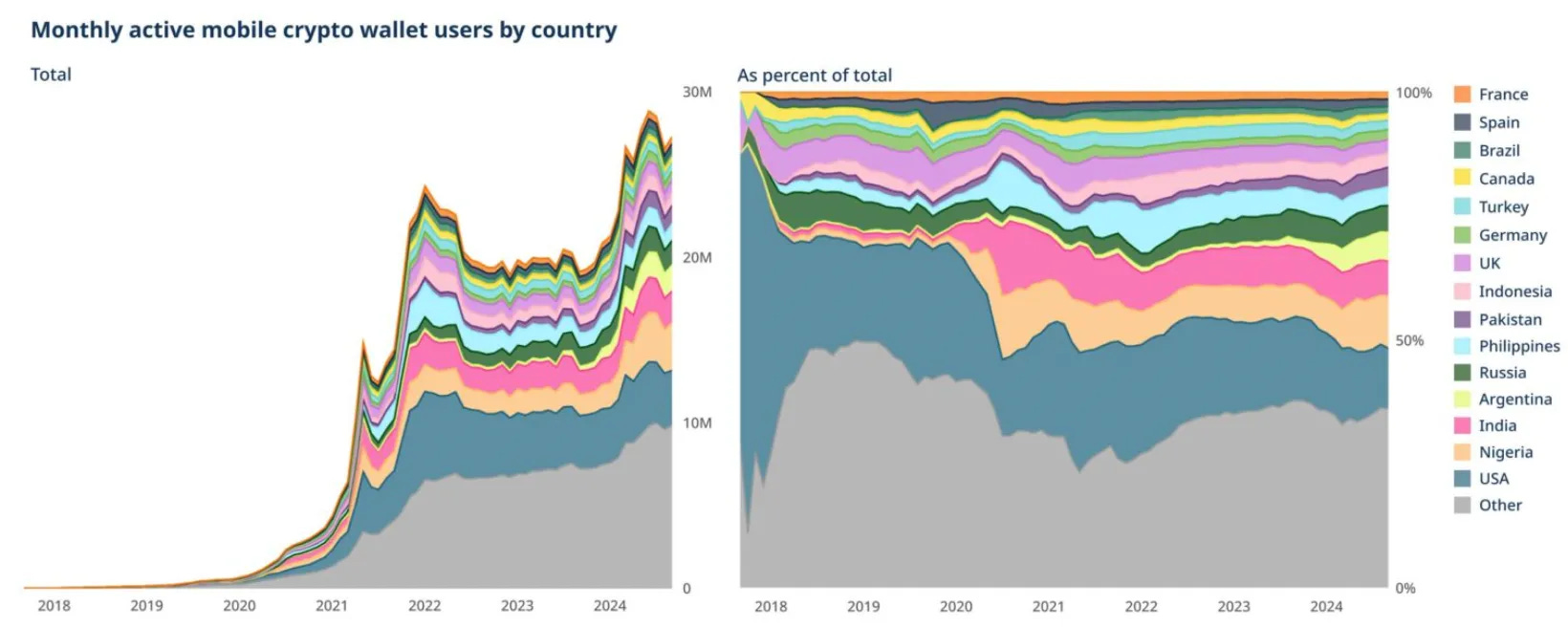

Nigeria is also one of the leading markets for mobile crypto wallet adoption, second only to the U.S. The country has actively worked toward regulatory clarity, including through incubation programs, and has seen significant growth in stablecoin use for everyday transactions, such as bill payments and retail purchases.

This high adoption has positioned Nigeria as a top global player in crypto, ranking second worldwide in the latest Chainalysis report. Unlike in many other markets, where crypto activity is largely speculative, stablecoins make up the largest portion of Nigerian crypto portfolios and are primarily used for non-trading purposes. Nigerian users report frequent transactions and the strongest understanding of stablecoins as a financial tool rather than just an asset class.

With inflation, remittances and financial access all driving adoption, Nigeria has become the proving ground for stablecoins in Africa. The country’s role in stablecoin infrastructure will shape how the technology evolves across the continent.

In December 2023, Nigeria’s lift of the central bank’s ban on banks serving crypto companies has also played a pivotal role in adoption. Since the banking ban was lifted, it has opened up a lot of possibilities for partnerships and smoother transactions. Building on this development, in June 2024, the Securities and Exchange Commission (SEC) of Nigeria introduced its Accelerated Regulation Incubation Program (ARIP), which now requires all virtual asset service providers (VASPs) to register and undergo an assessment before full approval. The industry is bullish on ARIP; it’s a shift away from uncertainty and a positive move towards regulatory clarity.

These policy efforts would allow companies in all industries to consider shifting from legacy payment rails to stablecoin infrastructure. And while compliant solutions are not elegant, each stablecoin adopter helps prove to incumbent businesses that stablecoins are a reliable, safe, regulated and improved solution to classic payments problems.

South Africa’s crypto market is booming with institutional and TradFi adoption

South Africa has positioned itself as one of the most advanced Web3 markets in Africa, supported by a progressive regulatory framework and strong institutional interest. The country has emerged as one of the continent’s largest cryptocurrency markets, receiving $26 billion in transaction value over the past year. Unlike many African nations where crypto adoption is primarily driven by retail users, South Africa is seeing increased institutional participation, with licensed firms and traditional financial institutions entering the space.

A key driver of South Africa’s crypto growth is its clear regulatory stance. The country has already classified cryptocurrencies as financial products, creating a structured legal environment that provides clarity for businesses and investors. In March 2024, South Africa approved 59 crypto operating licenses, paving the way for broader stablecoin adoption. By setting regulatory guardrails, the government aims to attract investment, protect users from cybercrime, and expand access to low-cost digital asset transactions.

Stablecoins are already becoming part of South Africa’s financial landscape, with two key Rand-pegged stablecoins—ZARP and ZARC—gaining traction. ZARP launched in 2021 on the OVEX crypto exchange, while ZARC went live in early 2023 and is available on the non-custodial crypto app SentiPay. As local stablecoins integrate into payment networks, they provide a bridge between traditional finance and digital assets, making it easier for South Africans to transact, save, and settle bills using stablecoins.

South Africa’s Intergovernmental Fintech Working Group is actively refining its approach to stablecoin regulation, with plans to officially classify stablecoins as a unique subset of crypto assets. This move aligns with the country's broader push for financial modernization and digital payments, ensuring that stablecoins are properly integrated into the financial ecosystem. The 2024 budget review further emphasized the government’s commitment to structural reforms, improved public financial management, and new policies focused on stablecoins and blockchain-based digital payments.

The growing institutional interest is also fueling discussions around bank-issued stablecoins. As traditional financial institutions explore stablecoin models, South Africa could soon see regulated, bank-backed digital assets that bring stablecoins further into mainstream adoption. With startups like VALR, Luno and Altify leading the way, South Africans are already using stablecoins to diversify investments, make payments and access financial services more efficiently.

With a well-developed financial sector, regulatory clarity and increasing integration between crypto and traditional finance, South Africa is becoming a leader in stablecoin adoption on the continent. As the government refines its policy framework and institutions deepen their involvement, the country is setting the stage for stablecoins to play a central role in its evolving digital economy.

Kenya is emerging as a stablecoin hub in East Africa

Kenya has long been at the forefront of financial innovation in Africa. From pioneering mobile money to embracing web3 early, the country has consistently leapfrogged traditional banking systems in favor of more efficient digital solutions. Now, Kenya is positioning itself as a key player in the stablecoin revolution, leveraging its strong fintech infrastructure, regulatory openness, and growing demand for alternative financial services.

One of Kenya’s biggest advantages is its deeply embedded mobile money culture. M-Pesa, launched in 2007 by Safaricom, has become the backbone of Kenya’s financial system, processing around 60% of the country’s GDP and reaching over 90% of the adult population. Its success lies in its ability to provide banking services without the need for a physical bank, allowing millions of Kenyans to deposit, withdraw, transfer, and even access credit from their mobile devices. Stablecoins are a natural fit in this ecosystem, offering users the ability to hold value in a stable currency and transact globally without friction.

Beyond mobile money, Kenya’s regulatory environment has been a major enabler of fintech and Web3 growth. Unlike many countries that have taken a restrictive stance on digital assets, Kenya’s Capital Markets Authority (CMA) has actively fostered innovation through a regulatory sandbox, allowing blockchain-based companies to test and refine their products.

The demand for stablecoins in Kenya is being driven by gaps in access to formal financial services. Small and medium-sized enterprises (SMEs) in particular face major hurdles in accessing credit, with Kenyan businesses seeking approximately $1.1 billion in loans in 2021 alone. Stablecoin-powered lending solutions could fill this gap, providing cheaper, faster, and more accessible credit options for businesses and individuals.

Kenya has also emerged as a global leader in tokenized private credit. According to RWA.xyz, Kenya ranks #1 worldwide in tokenized real-world asset lending, with $73.8 million in loans borrowed—outpacing much larger economies like India and Brazil. This reflects not only the high demand for alternative financing solutions but also the country’s ability to integrate blockchain-based credit models into its financial ecosystem.

With a mature mobile money landscape, progressive regulators, and increasing stablecoin adoption, Kenya is quickly becoming a key stablecoin hub in East Africa. As more fintech players build stablecoin-powered solutions, Kenya’s role in shaping the future of finance across the region will only continue to grow.

Projects driving the future of stablecoin adoption in Africa

Over the past three years of investing in the African market, we’ve seen a growing number of companies building around stablecoins, each playing a key role in driving adoption and innovation. Below is a list of some of the most notable players, along with key growth and fundraising numbers that highlight the sector’s rapid expansion.

Yellow Card: The largest and first licensed stablecoin on/off-ramp in Africa. Yellow Card allows users to seamlessly convert fiat to crypto and vice versa. In 2024, the platform doubled its annual transaction volume to $3 billion, up from $1.5 billion in 2023.

Conduit: Enables stablecoin payments for import-export businesses across Africa and Latin America. Annualized TPV surged to $10 billion in 2024, up from $5 billion in 2023.

Juicyway: A Lagos-based startup facilitating cross-border payments using stablecoins. Juicyway has processed $1.3 billion in total payment volume since 2021.

Bridge: Acquired by Stripe for $1.1 billion just two years after its launch in 2022, Bridge strengthens global stablecoin payment infrastructure. It serves most African payment companies, facilitating stablecoin payouts across Europe, the U.S., and Asia.

Jia: A blockchain-based fintech providing loans to micro and small businesses in emerging markets. In 2024, Jia’s cumulative loan originations surpassed $10 million, up from $2 million the previous year, delivering a 24% IRR with a 0.14% default rate.

Onboard: A global P2P exchange protocol that allows anyone, anywhere to access on-chain finance. Nestcoin raised $1.9 million in its last funding round to fuel the growth of its product.

KotaniPay: Provides stablecoin settlement solutions for businesses and users. Developing an API product that connects blockchains with local payment channels, In 2023, KotaniPay raised $2 million in pre-seed funding.

Accrue: Building a USD-stablecoin agent network to expand cross-border payment infrastructure. Secured $1.58 million in seed funding to scale operations.

Convexity: Developed cNGN, Nigeria’s first regulated stablecoin. The company has been engaging with the Central Bank of Nigeria since 2021 and received a provisional license from SEC Nigeria in 2024.

Honeycoin: A platform for cross-border remittances, bill payments, airtime purchases, and online spending. GTV surged to $500 million in Q4 2024, up from $40 million in the previous quarter.

Paycrest: Paycrest is a decentralized liquidity protocol enabling instant, low-cost payments powered by stablecoins. Additionally, they developed Zap, a dApp for seamless crypto-to-fiat payments, which was recognized as a winner in Base's global Onchain Summer Buildathon 2024. Today Zap is production ready as Noblocks which is the first interface for instant decentralized payments to any bank or mobile wallet, powered by a distributed network of liquidity nodes.

Haraka: A stablecoin-powered microcredit protocol targeting underserved entrepreneurs in emerging markets. Haraka leverages a reputation-based credit scoring system and has demonstrated early commercial validation through partnerships with Grameen and Mercy Corps.

Many of these companies have experienced significant growth over the past two years and are at the forefront of stablecoin innovation in Africa. This list is by no means exhaustive—if you’re building a stablecoin project in Africa, we’d love to hear from you.

Stablecoins are redefining finance in Africa

Stablecoins are fundamentally transforming the financial landscapes of emerging markets by providing accessible, efficient and reliable alternatives to traditional banking systems. Unlike the institutional-driven adoption seen in Western economies, emerging markets such as Sub-Saharan Africa are experiencing grassroots growth fueled by retail users engaging in small transfers, remittances, peer-to-peer payments, and value storage.

The past few years have proven that stablecoins are not just an alternative but the inevitable future of money in Africa. Their ability to bypass broken financial rails, provide access to stable value, and enable instant, low-cost transactions has made them a critical tool for individuals, businesses, and even institutions. As more infrastructure is built, and regulatory clarity improves, stablecoins will only become more deeply embedded into Africa’s financial fabric.

The momentum is undeniable—countries like Nigeria, Kenya, and South Africa are leading the way, each leveraging stablecoins in unique ways to drive financial inclusion and economic growth. But this is just the beginning. The next phase of stablecoin adoption will be shaped by builders, investors, and policymakers who recognize the massive opportunity at hand. New projects will emerge, deeper integrations will be made, and stablecoins will continue to evolve to meet the needs of millions.

We would like to express our gratitude to Zach from Jia, Yele from Nestcoin, Will from Haraka and Francis from Paycrest for generously sharing their valuable insights which have been integrated into this article.

Hashed Emergent may have or can invest in companies mentioned in this article. This content is for informational purposes only and should not be construed as investment advice. Please do your own research before making any investment decisions.