Blockchain Economics: How much does it cost to run your own chain?

Launching a blockchain is becoming increasingly convenient due to improvements in its tech stack. This article explores these developments and their impact on the cost of running a blockchain.

There has been a significant surge in the launch of new Layer 2 (L2) solutions over the past year, driven by technological advancements, the development of unique go-to-market strategies, a focus on specialized use cases, and strong community engagement. While this development is encouraging, the primary challenge remains scaling these blockchains in a more cost-effective manner. Running an appchain has emerged as a key solution, as appchains can manage the costs of operating a blockchain through initiatives across the modular infrastructure stack.

While specific initiatives by the L1 – Ethereum have made it significantly cheaper to transact on blockchains, there has also been a strong push by major rollups and infrastructure providers to further enhance scalability and unlock use cases that are currently prohibitively expensive to be executed on chain.

We can classify and analyze these developments through the lens of a) L1 initiatives, b) L2 initiatives, and c) Modular infrastructure initiatives, all of which have meaningfully contributed to reducing barriers to entry for transacting on chain.

In recent times, we have seen various upgrades on Ethereum such as EIP 1559 and 4844 which have lowered costs and improved scalability.

We shall first take a look at the L1 initiatives that have contributed to rationalizing costs of transacting on the Ethereum chain in the form of EIPs such as EIP 1559 and EIP 4844 (Dencun Upgrade). While EIP 1559 introduced the concept of base fee + tip / priority fee and congestion based dynamic pricing (see Exhibit 1) providing users a better mechanism to estimate costs and transact over the network depending on their priorities and network congestion, EIP 4844 brought a new kind of transaction type to Ethereum by introducing the concepts of Blobs (Binary Large Objects) which provide a drastically cheaper alternative for L2s by allowing them to store data in Blobs instead of costly callData while settling transaction on the L1.

The implementation of Blobs has led to a dramatic reduction in transaction costs due to both reduction in storage costs per byte as well as expanding capacity per block as Blobs unlike callData don’t compete for gas with Ethereum transactions and are not stored permanently, getting removed from the blockchain after ~18 days.

Blobs are 4096 field-elements of 32 bytes each with a long-term maximum of 16 Blobs per block thereby providing ~2 MB (4096 * 32 bytes* 16 Blobs per block) of maximum additional capacity which can be achieved by starting low (currently at 0.8 MB with target size of 3 blobs per block and a maximum of 6 post EIP 4844) and reaching capacity over multiple network upgrades in the future. Given the historical benchmark of 2-10KB of callData per block, EIP 4844 implies a theoretical increase of up to 384x.

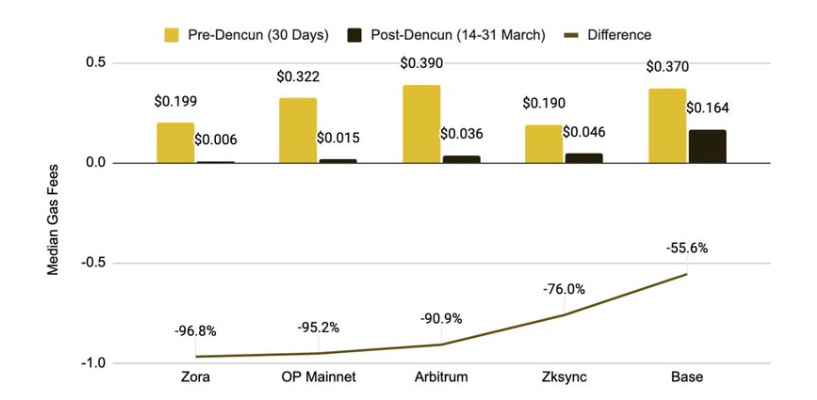

In practice, many L2’s fees decreased by more than 90% following the implementation of EIP 4844 (see Exhibit 2). However, relying solely on these upgrades is insufficient for Ethereum to achieve greater scalability. In a world with thousands of rollups, transaction costs are likely to spike due to increasing demand for storage space as mass adoption occurs on-chain.

As L2s move execution off-chain to cut costs while maintaining security, industry initiatives like open-source frameworks and revenue-sharing models are shaping the competitive “L2 stack wars”.

The advent of rollups in the previous cycle aimed to substantially reduce costs for operating on chain by moving execution off the main chain while still deriving security from it using various proof types. While optimistic roll ups allow for a single honest entity to submit a "fraud proof" and earn a reward for identifying a misbehaving sequencer, ZK (zero-knowledge) rollups use zero-knowledge proofs to prove that the L2 chain has updated correctly.

Rollup operators perform various tasks including:

Sequencing: Organizing end user transactions in order, grouping them and occasionally posting these grouped batches to the L1

Execution: Storing and executing operations and updating the state of the rollup

Proposing: Proposers update the state root of the rollup on Layer 1 periodically, this is important to ensure blockchains remain trustless and verifiable by all

State Root Challenge: Submitting evidence of state root fraud and challenging the state root on Layer 1 (applicable only to Optimistic Rollups)

Proving: Generating validations for each state root status update from the rollup to L1 (applicable only to ZK Rollups)

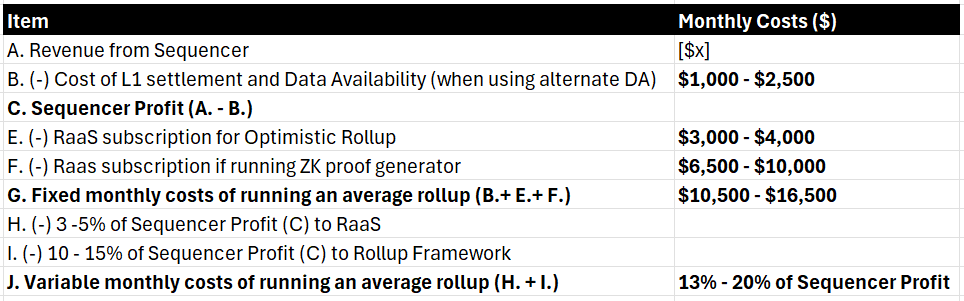

They make revenue through transaction fees paid by the users (sequencer revenue) and potential MEV they can extract though it is important to note that currently MEV is not extracted as a policy choice. Their costs can largely be attributed to L2 (operational cost) and L1 (data availability and settlement) costs (See Exhibit 3). Organizations looking to launch their own chain would ideally only want to do so if they expect to generate higher transaction fees than the cost of such an initiative.

Base layer networks such as Ethereum tend to charge more for computation and storage as a majority of the nodes need to be able to sync and validate a chain. However, in a rollup, the chain is considered safe even if one honest entity is able to validate the chain. Consequently, rollups charge less for computation and storage but more for the cost of “rolling up” transactions into batches and publishing them to an L1 resulting in L1 costs forming up to 98% of the cost base for L2s (See Exhibit 4) prior to the introduction of EIP 4844.

Apart from the base level optimizations, there has been a strong push by L2s to further bring down costs, these initiatives are what we described at the start of the article as Layer 2 initiatives and they can largely be categorized under two buckets – industry aligned or company aligned.

Industry aligned initiatives include actions that allow new players to build their own chains by open sourcing the L2 technology stack (rollup framework). While this wave of initiatives was led by optimistic rollups through the launch of OP Stack and Arbitrum Orbit, other mature L2s including Polygon (Polygon CDK), ZK Sync (ZK Stack) and Starkware (Madara Stack) have followed suit by providing or announcing the open sourcing of their proprietary technology for enabling mass adoption.

Company aligned initiatives include efforts by these chains to reduce costs but accrue value to their respective tokens via direct revenue / profit sharing models or indirectly through second order effects of expanding their ecosystems. Optimism’s Superchain vision, Arbitrum’s Expansion Program, Polygon’s Aggregation Layer, ZK Sync’s Elastic Chain are examples of such initiatives. The specifics of these programs may differ but the common theme across all these is the prevalence of an interconnected network providing for enhanced interoperability, communication across multiple rollups and shared critical infrastructure in the form of a shared base layer for data availability, a shared bridge, aggregated proofs (only for ZK chains) etc. to further capital efficiency – a problem that still plagues the current Ethereum ecosystem with fragmented liquidity and broken interoperability among rollups. However, these stacks also allow individual chains to retain their unique customization basis their requirements across parameters such as block times, withdrawal periods, finality, token usage, gas limit etc. thereby removing the disadvantages of being on a common chain in the form of high gas costs and latency due to the traction on other applications.

Though these individual ecosystems are focused on growth and adoption, we have started seeing monetization come through for more mature players such as Optimism and Arbitrum.

Optimism levies a fee of 2.5% of overall sequencer revenue or 15% of sequencer profit (sequencer revenue – L1 costs of settlement and data availability) from players who are looking to be part of its Superchain. Arbitrum charges 10% of sequencer profit from players launching an L2 using its stack while ZK rollup stacks including Polygon CDK, ZK Stack are free to use but will likely have sustainable economics built in as they evolve and gain traction.

The official “L2 stack wars” have started with all the ecosystems vying to onboard marquee projects (See Exhibit 5) via unique strategies. Optimism announced $22M in grants to Superchain builders providing them with airdrops retrospectively across usage and engagement parameters while ZK Sync offered $22M to onboard Lens from Polygon onto its stack. Arbitrum made it free for anyone to use its stack if they launch as an L3 on Arbitrum (L3 chains are chains that use L2 as a settlement layer instead of Ethereum) as it benefits from heightened L3 activity as these L3 chains will end up paying settlement costs to Arbitrum throughout their life cycle.

RaaS and alternative settlement and data availability solutions have redefined blockchain cost structures with future innovations in modular infrastructure poised to drive further savings.

Despite the availability of these technology stacks, running a blockchain involves a lot of operational overhead, manpower, expertise and resources to run. Builders looking to attract end users on chain do not want the distraction of dealing with the running and maintenance of the chain infrastructure and instead want to focus on core business activities.

This problem statement led to the proliferation of RaaS (Rollup as a Service) providers who work with these builders and abstract away the complexities of operating their chains using the frameworks / stacks of the mature L2s as discussed earlier. They provide services such as handling node operation, software updates, infrastructure management along with providing products like sequencing, indexing, and analytics. RaaS providers have taken different approaches to capturing market share, while some are ecosystem aligned with certain L2s, the others follow a more framework agnostic approach providing integrations across all ecosystems. Conduit and Nexus Network have aligned with optimistic roll ups such as Optimism and Arbitrum while Truezk, Karnot and Slush are focusing on ZK chains. On the other hand, Caldera, Zeeve, Alt Layer and Gelato provide integrations across both optimistic and ZK rollups.

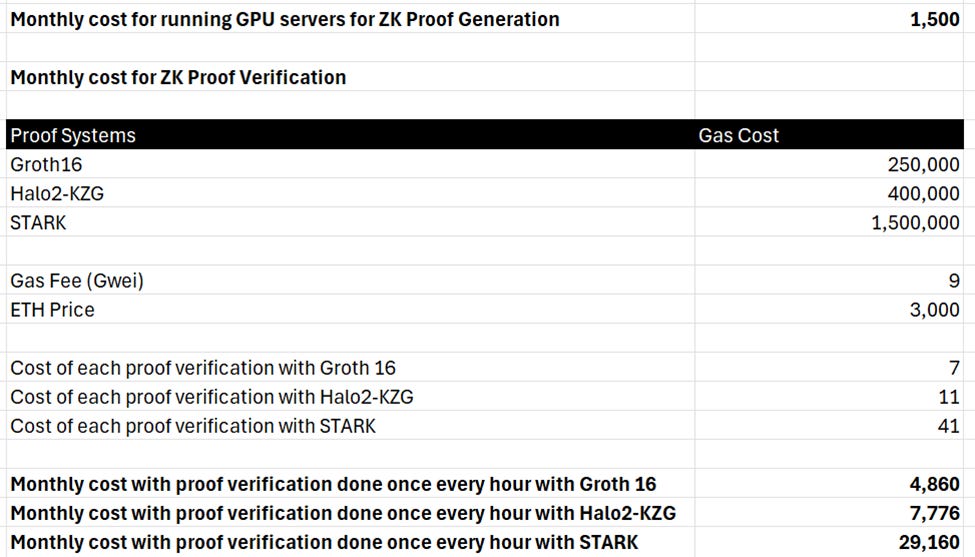

The typical business model for these providers involves a fixed fee in addition to a share of the sequencer profit. Monthly subscriptions for running optimistic rollups generally range from $3,000 to $4,000, whereas the costs can more than double to $9,500 to $14,000 for running ZK rollups due to the intensive compute required to generate ZK proofs and the extremely high cost of proof verification (see Exhibit 6 for further details). Additionally, a sequencer profit share of 3-5% is levied to align incentives between the RaaS providers and the rollups, allowing them to capture monetary upside as these chains gain traction.

Caldera is exploring a different model with its Metalayer vision, which involves only a variable sequencer profit share of 2% and no fixed costs, aiming to enable interoperability across chains using Caldera in both optimistic and ZK stacks.

It is important to note that the dynamic nature of the industry and the efforts of the teams working on these stacks particularly on the ZK side is likely to result in further compression of the subscription costs charged by the RaaS providers. Additionally, pricing may not be standardized initially across applications as larger consumer facing applications may be able to negotiate better economic sharing agreements with infrastructure providers due to the paucity of strong consumer web3 businesses.

As mentioned earlier, the largest expense for a rollup is the L1 costs i.e cost of data availability and settlement. The L1 costs for a standard rollup processing 100M transactions could be as high as $25,000 a month making L1 settlement a viable option only for the largest / most utilized chains in the ecosystem. The need for alternate settlement and data availability solutions has led to dedicated players optimizing costs and performance on these layers. Alternatives to Ethereum on data availability include Celestia, Near, EigenDA while the mature L2s discussed earlier aim to become the settlement layer for rollups which can be classified as L3s. These players have reduced settlement and data availability costs by orders of magnitude for rollups. Exhibit 7 provides a rough sense of cost savings to rollups if they would have posted callData to Celestia instead of Ethereum. It is worth highlighting that the delta in cost savings increases exponentially as transaction volume increases.

In addition to the cost of data availability, there is an additional cost of settlement that is required wherein Celestia posts a pointer on Ethereum that can be traced to the relevant block on Celestia (referred to as additional cost of settlement in Exhibit 7) to guarantee the ordering and integrity of the data being posted on Celestia.

The development of specialized players across the modular infrastructure stack in the form of alternate data availability and RaaS providers are what we can collectively refer to as Modular infrastructure initiatives. There are other verticals under this category that are exploring further cost optimizations including shared sequencing (Espresso, Astria, Radius), proof aggregation (Nebra, Electron) etc. These are currently in the early stages of development, and we expect costs to keep coming down as the industry matures.

While the costs of operating on chain have drastically reduced, web2 founders should conduct a thorough cost benefit analysis before deciding on launching their own chain.

Web2 founders should carefully assess the cost-benefit of launching their own chain, as despite reducing on-chain costs, these will likely be benchmarked to Web2 standards.

The fully loaded cost for running a chain depends upon the specific usage requirements of each chain but we can broadly estimate the costs for an average optimistic or ZK chain utilizing alternative data availability solutions tracking 2M transactions monthly as shown in Exhibit 8.

Despite various optimizations at the industry as well as individual chain level, the monthly financial commitment required would include total costs of $10,500 - $16,500 for ZK rollups and $4,000 - $6,500 for optimistic rollups in addition to up to 20% share of sequencer profit once the chain starts registering gains.

The three broad categories of initiatives as highlighted in this article will be key to democratizing access to the industry with the end goal of reducing the gap between costs and convenience of running a decentralized application vs web2. It is critical for builders to conduct a cost benefit analysis of running an independent chain vs being built on top of existing chains depending on their end user needs, product priorities, performance metrics required for their use case and their existing traction.

We recognize the need to build solutions that are diminishing the costs and performance differences between web3 and web2 infrastructure as social preference for using decentralized systems is not compelling enough to expand the web3 gamut. This challenge remains a key bottleneck to enable mass adoption of blockchains, and we are excited to meet founders building in this space!

We would like to express our gratitude to Dr. Ravi from Zeeve, Mayank from Nexus Network, Raghu from Rabble, Rafael from Numia, Apoorv from Karnot, Shumo from Nebra, Garvit from Electron and Yush from Lysto for generously sharing their valuable insights which have been integrated into this article.

Hashed Emergent may have or can invest in companies mentioned in this article. This content is for informational purposes only and should not be construed as investment advice. Please do your own research before making any investment decisions.